Pakistan’s Rising Palm & Soybean Imports: Understanding Key Drivers and Challenges[1]

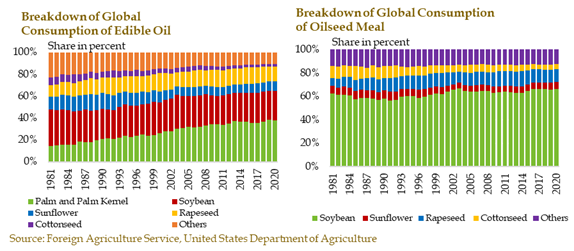

Pakistan’s imports of palm and soybean products have risen 55 percent in 1HFY22, following a 47 percent increase in FY21. While this recent growth stems from soaring international commodity prices, the overall trend is not a new phenomenon. Combined imports of palm and soybean have more than doubled over the last twenty years, rising to 7.1 percent of total imports in FY21, amid waning reliance on domestic sources (sunflower, canola, & cottonseed) for edible oil and meals for animal feed.

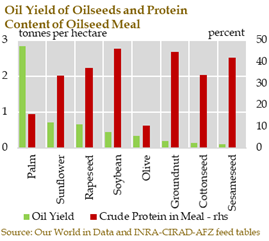

Palm and soybean are the world’s most used crops for edible oil and oilseed meals because of their high resource-use-efficiency, measured in terms of oil yield per hectare for oil, and protein yield in the case of meals. The former is important to meet the requirements of a growing human population and rising per capita consumption. The latter is important to feed ruminants, poultry, and aquatic foods, since protein-based meals enable faster and healthy growth of these animals.

demand side drivers

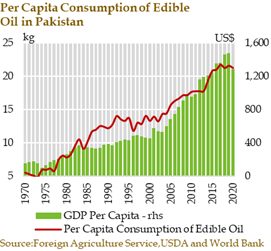

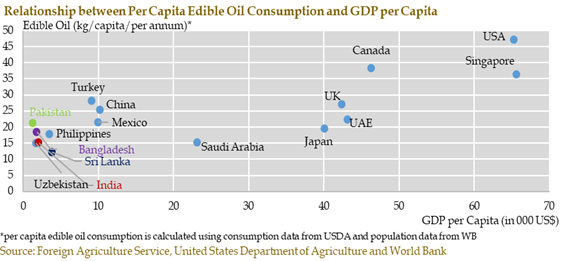

In Pakistan’s case, the demand for edible oil is being driven both by growing population and rising per capita consumption. Contributing to the latter is a dietary preference for higher oil use, as suggested by cross country comparison of per capita edible oil consumption. And because palm oil is generally cheaper than other types of edible oils, Pakistan imports palm oil the most compared to other oils.

Similar demand drivers are at play in the case of oilseed meals. Growing population and rising per capita income are stoking the demand for poultry, livestock and farmed aquatic foods, which in turn creates a demand for oilseed meals as key components of animal feed. And following the fast paced modernisation of the domestic poultry industry, the demand for soybean meals has increased manifold. The growing modernisation of the dairy and meat industry, as evidenced by an increasing number of corporate meat and dairy brands, is also creating a demand for soybean-based meals.

supply side drivers

Pakistan’s government has planned, and rolled out various programs and initiatives to increase oilseed production over the last six decades. Starting from the first 5-year Plan to the most recent one, the importance of increasing oilseed output has been recognized both to reduce the import bill, and to improve human and animal nutrition. Whilst most proposed measures have revolved around sunflower and rapeseed/canola, soybean has also featured in the Plans since the 1960s, whereas oil palm plantations have only recently garnered attention.

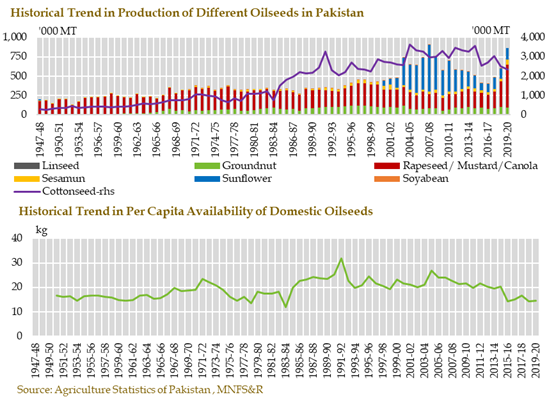

Despite support measures recommended in various Plans, the cultivation of oilseed crops stagnated in the first four decades after 1947, in sharp contrast to the rest of the agriculture sector. In recent years as well, the production of oilseeds crops did not increase as targeted while yields remained weak in comparison to other countries. During the last 15 years, the local production of edible oil has declined by 1.2 percent per annum, while demand per capita has increased by 2.3 percent, leading to increasing reliance on imports.

Overarching challenges to oilseed production

Among the factors responsible for the low production of oilseeds in Pakistan are: limited research, thinly spread over a large number of institutes; deficiencies in agriculture extension; absence of support prices; challenges to crop marketing and procurement challenges leading to weak linkages in value chains; and inefficient oil extraction in villages and small towns.

Low profitability and the falling prices of palm oil imports have also contributed to falling domestic oilseed production. The lack of policy focus has also led to limited seed availability, both in terms of varieties suitable to the local environment, and the quality needed for optimal productivity. In addition, there are constraints to best farming practices, such as a shortage of oilseed-specific planting, harvesting and threshing machinery, and non-adoption of other recommended production technology. Lastly, since oilseeds compete for land with other crops that are important for food grain sufficiency and exports, the failure to achieve potential yield in food grain and other major crops leaves lower acreage available for cultivation of oilseeds.

The lack of policy focus stems in part from institutional challenges. Initially, in 1977, the Pakistan Edible Oil Corporation was set up to manage oilseeds policy but this was dissolved after two years of spadework. It was replaced by the Seed Division established in Ghee Corporation of Pakistan. The division was abolished in 1993. In 1994, Pakistan Oilseed Development Board (PODB) was set up with a comprehensive mandate to increase oilseed production. After a series of suspension, closure, reduction in mandate, and reactivation since 1994, the PODB was restored to its previous status in June 2021 under the new name of Pakistan Oilseed Department (POD). However, since the 18th Amendment, little support exists to provinces from POD whereas provinces do not have oilseed specific institutions.

prospects of local palm & soybean production

Oil Palm

After a feasibility survey of 3.86 million hectares in Sindh in the mid-90s, the National Agriculture Research Council (NARC) suggested that some parts of the country’s coastal belt were suitable for oil palm plantations. Accordingly, oil palm cultivation was initiated in 1998 as a pilot project. However, after some promising years, the pilot project faced farm management issues and operational bottlenecks. On the whole, the project was not closely monitored, partly because of institutional challenges such as those discussed earlier.

More recently, in 2017, a new pilot project by Sindh Coastal Development Authority (SCDA) has shown encouraging results, though on a small scale of only 50 acres. The SCDA suggests relying on irrigated water to explore the potential of oil palm plantation. However, detailed scientific studies have not yet been carried out in Sindh or Baluchistan. This needs to be done urgently as progress in agriculture techniques (such as introduction of more resistant varieties vis-à-vis climate and soil) or change in environment (such as water drainage, water tables) necessitates reassessment of land suitability every 10-15 years.

The success of government intervention in oil palm plantations in Malaysia and Indonesia suggests that oil palm may be explored as an irrigated crop along the coastal belts of Sindh and Baluchistan, as done recently in India. To ensure that pilot projects can test the theoretical potential, good farm management would be critical. In addition, a strong palm-specific institutional set up may be needed to work in close collaboration with leading private sector investors, in line with the strategy adopted by Malaysia and Indonesia. To this end, a government-to-government or government-to-business partnership with China may be explored under the China Pakistan Economic Corridor.

However, even in the most optimistic scenario, palm plantations may not start yielding adequate quantities of oil before 10-15 years. This is because research, trials, setting up of institutions, and project implementation are long-term endeavors requiring consistent effort. The palm tree itself attains maximum fruiting in 4 to 7 years and continues to fruit for 15 to 30 years.

Soybean

Although policy measures for soybean had been recommended as early as 1955, a support price for the crop was not announced until 1978. Even then, the crop’s progress remained weak, due to the absence of coherent research and production policy for soybean vis-à-vis farmer awareness, non-existent value chain, seed development, production technology and procurement policy.

Following the increase in demand for soybean meal by the poultry feed industry, the pace of research has recently started to pick up, where the biggest crop-specific challenge is the availability of sowing seeds suitable to Pakistan’s generally hot climatic conditions. This warrants further investments in seed varieties better suited to the climatic conditions of the country’s major cultivable regions, particularly south Punjab and Sindh. In light of this, initial seed trials separately done by the Oil Research Institute, Faisalabad in 2018-19 and the NARC show some promise. Accordingly, in the medium term, Pakistan may be able to grow 0.5 million tons of soybean, which is about 20 percent of the country’s FY21’s soybean import quantity.

However, to realize this potential, the overarching challenges to oilseed crops noted earlier would need to be addressed. Particular focus is needed on farmer awareness; farm management; procurement mechanisms; and making oilseed cultivation a profitable endeavor for farmers and other players in the value chain. In addition to desired quality, the availability of soybean’s sowing seeds is critical to reap this potential since soybean requires much higher quantities of sowing seeds at the rate of 30-35 kilogram of per acre, compared to 2-3 kg/acre in the case of sunflower and rapeseed/canola.

final remarks

Given current trends in population, and necessary modernization of poultry, livestock, and aquatic foods industry to meet rising domestic meat consumption and export potential, Pakistan’s demand for edible oil and meals is likely to continue growing over the next few decades. In the short to medium term, a policy focus on increasing the production of canola and sunflower is necessary, and currently in the process of being rolled out. Sunflower and rapeseed/canola already have roots in the country. Meanwhile, palm offers no potential in the short to medium term and soybean’s potential hinges on a variety of policy reforms.

In the longer run, however, different considerations apply. The oil and protein yield per hectare of canola, sunflower and sesame are significantly lower than that of palm and soybean, which is an important consideration in light of scarcity of land, water and other resources. Over the long-term, therefore, there is an urgent need to invest in research, development, promotion, production and procurement mechanism for oil palm plantation and soybean crops.

Agriculture production policy depends on a variety of complex and interwoven factors, the diversity of which implies that no country can become completely self-sufficient in all the crops it consumes. While recognizing this, the realities of growing palm and soybean imports warrants technical research, feasibility studies, and concerted deliberations among federal and provincial governments, as well as private and public stakeholders to at least assess whether or not Pakistan has the potential of growing these two crops. If there is potential to grow them, consistent policy and institutional support will need to be provided to make that transition successful.

The writer works as Senior Economist at the State Bank of Pakistan (SBP).

[1] This article is a summary of key findings of the SBP’s Special Section published in the State of Pakistan’s Economy report for 1QFY22. For details, read “Pakistan’s Rising Palm & Soybean Imports: Understanding the Drivers and Challenges to Domestic Oilseed Production,” available here.