Macroeconomic Crises and Economic Recovery: the labor market angle[1]

Since 2000-01, Pakistan has negotiated six IMF programs to address balance of payments crises[2]. The programs have resulted in major adjustments that include sharp devaluation of the rupee and cut back in public expenditure including public investment. A slowing down of economic growth and inflation have followed the adjustments and are well documented (see, for example, Nabi and Nasim)[3].

There is little discussion, however, on the impact of adjustments on the labor market, especially wages. Have real wages fallen thus shifting the burden of adjustment to workers? How has overseas migration to higher wage economies affected the outcomes? What does that imply for international competitiveness and export led growth that will anchor sustained recovery? This note explores these questions.

Inflation

We start with inflation since that (as a tax on wages) can be an important outcome of exchange rate adjustment, a key stabilization measure.

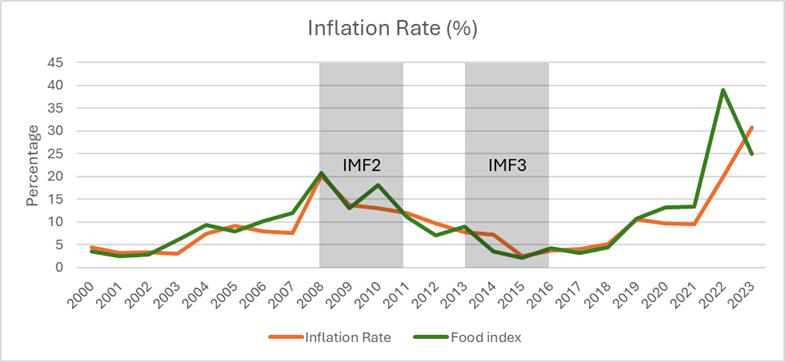

Figure 1 tracks overall and food inflation between 2000-01 and 2023. Inflation ratcheted up after three of the four IMF programs, sharply so in IMF4 (2019-22) when inflation peaked at 38 percent. The sharp increase in inflation was also due to the COVID effect. Correction in global commodity prices explains the low inflation following IMF 2 (2008-2011). Food inflation has closely tracked core inflation. It is important to note that inflation in this period was only partially cost-push (because of exchange rate adjustment); there were also episodes of loose fiscal and monetary policies (not consistent with the IMF program).

Figure 1: Inflation and IMF supported stabilization programs (since 2000-01)

Source: Pakistan Economic Survey & Macrotrends

Note: IMF1 = Growth Facility (PRGF) (December 6, 2001 to December 5, 2004)[i], IMF2 = Standby Arrangement (November 24, 2008 to September 30, 2011), IMF3 = Extended Fund Facility (September 4, 2013 to September 30, 2016), IMF4 = Extended Fund Facility (July 2019 to October 2022);

Wages

The evidence on how stabilization is playing out in the labor market is presented first by focusing on nominal wages for different categories of skills in theLabor Force Survey (LFS)[4].

LFS covers 99,904 households and provides information on labor force participation rates, sectoral employment by different skill categories and monthly income. The income data reported in Household Income and Expenditure Survey (HIES) closely matches that reported in LFS. The most recent available survey data are for 2020-21. This allows us to assess the impact of stabilization efforts under three IMF programs (IMF1, 2 and 3) that were negotiated int the period 2000-2021.

The impact on wages is assessed by grouping workers in three skill categories:

Low income skills: occupations are agriculture, forestry and fishery workers, craft and related trade workers, plant/machine operators and assemblers and elementary occupations (unskilled informal workers).

Middle income skills: occupations are technicians, clerical support workers and services and sales workers.

High income skills: occupations are managers and professionals.

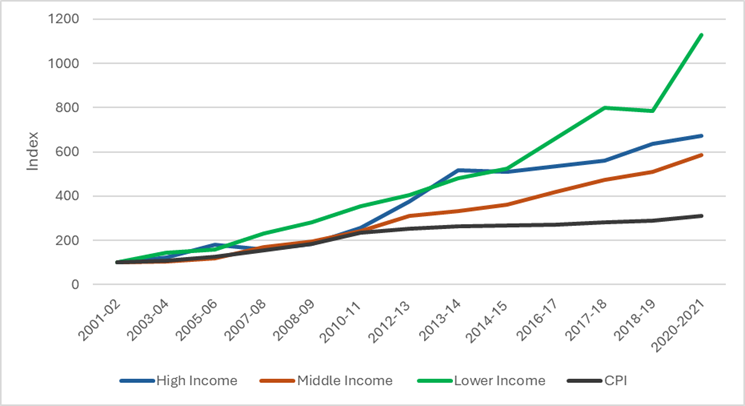

To assess the trend in real wages, an index of nominal wages was constructed for all skill categories with the year 2000-01as the base. The nominal wage index graphs corresponding to the three categories of skills were compared with the CPI for the same period. The graphs are shown in Figure 2a.

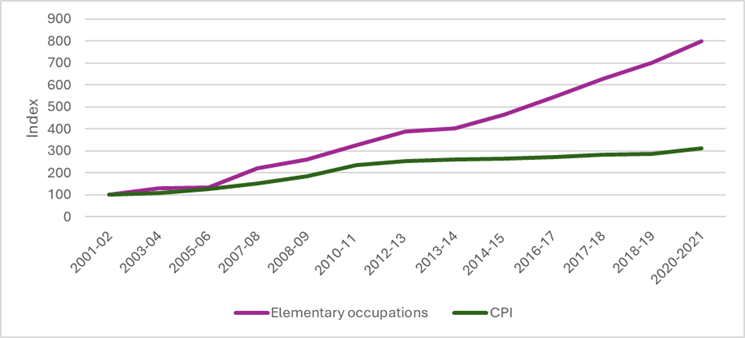

Between 2000-01 and 2021, CPI index increased from 100 to just over 300. However, the index of nominal wages for all skill categories increased much more: middle income skills index increased to 600, high income skills to nearly 700 and low income to 1150. Thus, real wages of all skill category workers increased substantially in this period. The substantial increase in real wages is true also for workers in elementary occupations (that include occupations in the informal market) as shown in Figure 2b.

Figure 2a: Nominal wage and CPI trend for different skill category of workers.

Figure 2b: Nominal wage and CPI trend for least skilled workers (Elementary workers) .

Job outcomes

The substantial increase in real wages would suggest strong job growth and tightening of the labor market following successful stabilization. However, barring a few years in 2000 – 2022, GDP growth was modest and investment sluggish, so demand for labor was weak. Corroborating this is the direct evidence on job growth reported in the labor force survey which shows that most of those seeking jobs were absorbed in the informal labor market (Figure 3a). The gap between those entering the labor force and available formal jobs widened (Figure 3b).

Figure 3a. Job growth in formal and informal economy

Figure 3b: The growing job gap

So, what is going on? Why have real wages increased so much at a time of poor job creation? This requires a look at the larger labor market in which a high proportion of Pakistani workers operates and which affects wage formation in Pakistan.

Worker migration overseas[5]

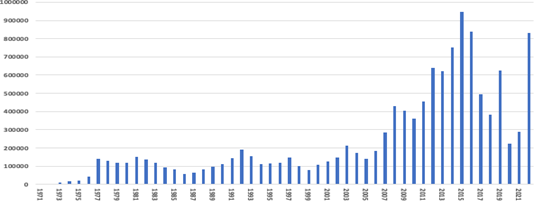

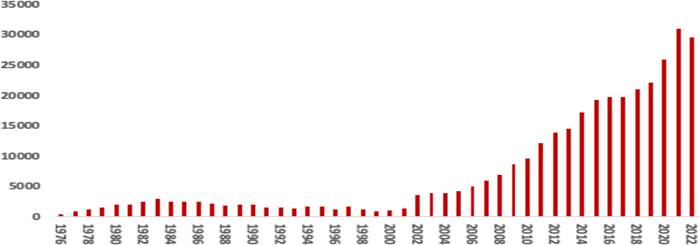

Worker overseas migration increased substantially in the late 1990’s coinciding with poor performance of the economy and rise in labor demand in the oil rich Gulf region. Furthermore, the share of skilled workers among the migrants is rising[6]. Increased worker migration has resulted in a sharp rise in remittances (Figures 4a and 4b) to around 7 percent of GDP (nearly 9 percent now).

The opportunity to work overseas when the domestic economy is not creating sufficient jobs, especially if the jobs pay considerably higher wages, has had a salutary impact on the welfare of low income households receiving remittances. Pakistan’s stellar poverty reduction in the last three decades and growth in the size of the middle class is largely due to remittances.[7]

Figure 4a: Emigration from Pakistan, 1971-2022

Source: Bureau of Emigration and Overseas Employment, Pakistan

Figure 4b: Remittances, 1976-2022

Source: World Development Indicators

There is, however, the other side of the story. A large body of research shows that overseas migration and remittances have Dutch disease consequences for the labour exporting countries. Chami et. al. (2006)[8] argue that while employment declines anyway during economic downturns, remittances intensify this effect by inducing a reduction in the willingness to work of recipients. This deepens the amplitude of recessions. In a different vein, Chami et. al. (2005)[9] point out that compensatory remittances cushion income loss during bad states of nature. While this increases recipients’ welfare, it reduces their incentive to put effort into mitigating the risk of negative income shocks in the first place and this makes such shocks more likely.

The adverse labour market consequences have also been reported in Pakistan. Kozel and Alderman (1990)[10] found that remittances negatively affect male labour force participation and hours worked in urban areas of Pakistan. Combining the two effects, there was a dramatic decrease of 14.3 hours per week on male labour supply. A more recent study (Jafari et al, 2024, cited above) on remittances induced Dutch disease in Pakistan also reports a negative correlation between remittances (that fuels the expectation of substantially higher wages in the overseas market) and labour force participation.

Two factors might be at play in the labour market. One, access to overseas jobs fuels expectation of higher wages in both formal an informal market but perhaps more so in the former and, two, labour market rigidities (differences in education, skills and commuting difficulties) sustain the wage gap between formal and informal jobs.

Policy response

High sustained growth in a high wage labor market requires raising worker productivity. Philippines did that and has tempered the labor market manifestations of Dutch disease associated with remittances[11]. Raising productivity requires concerted policy response across a broad front. A recent World Bank study[12] argues that firms that attract higher foreign direct investment, those exporting products/services in the international market and those hiring female workers have higher worker productivity and thus are more likely to grow in a high wage setting. A well-coordinated, evidence based policy response especially to attract foreign direct investment and resuming export led growth will thus be key.

This has implications for structural reform underpinning the IMF stabilization programs. Productivity improving public expenditure, and private investment attracting public investment, must be protected to lower unit labor costs to anchor sustained export led growth. Complementary lending by World Bank and the ADB must strengthen targeted initiatives to that end. This includes addressing labor market rigidities that sustain the wage gap between formal and informal jobs.

[1] The note has befitted from comments by Naved Hamid (IGC/CDPR and Lahore School) , Anjum Nasim (IDEAS), Shahid Yusuf (CGD, GWU), Najy Benhassine, Tobias Akhtar Haq and Adnan Ghuman (World Bank).

[2] Growth Facility (PRGF) (December 6, 2001 to December 5, 2004)[2], Standby Arrangement (November 24, 2008 to September 30, 2011), Extended Fund Facility (September 4, 2013 to September 30, 2016), Extended Fund Facility (July 2019 to October 2022); Standby arrangement (2023 – 2024); Extended Fund Facility (2024 – )

[3] Ijaz Nabi and Anjum Nasim, “Pakistan: How to Live Within Means addressing chronic fiscal deficits”, Vanguard press, 2025

[4] The survey has been conducted by Pakistan Bureau of Statistics since 1963.

[5] The discussion in this section draws on S. Jafari, AK Maak, I.Nabi, I.Qureshi, “Are Overseas Remittances a Source of Dutch Disease in Pakistan?” (March, 2024).

[6] According ILO (ILO, 2016), in 2015 almost all (99.9%) of Pakistani workers in the GCC were male; skilled workers constituted the largest category (42%), followed by un- and low-skilled (39%), and semi-skilled (16%). High-skilled and highly-qualified workers accounted for only 3%.

[7] World Bank

[8] Chami, R., (2006): Beware of emigrants bearing gifts: Optimal fiscal and monetary policy in the presence of remittances, IMF Working Paper 06/61, International Monetary Fund, Washington DC.

[9] Chami, R., C. Fullenkamp and S. Jahjah (2005): Are immigrant remittance flows a source if capital for development? IMF Staff Papers 52(1), 55-81.

[10] Kozel, V. and H. Alderman (1990): Factors determining work participation and labour supply decisions in Pakistan’s urban areas, Pakistan Development Review, 29(1), 1-18.

[11] Bayangos, V. and K. Jansen (2011): Remittances and competitiveness: The case of Philippines, World Development 39(10), 1834-1846.

[12] World Bank (2022): From swimming in sand to high and sustainable growth, mimeo, World Bank, Washington DC.