2023 was one of the worst years in Pakistan’s economic history. Growth declined to 0.3 percent, while average headline inflation soared to 29.2 percent, close to all-time highs and lows, respectively. In response to rising inflation, the Monetary Policy Committee (MPC) of the State Bank of Pakistan (SBP) raised the policy rate by 825 basis points to 22 percent and maintained it at that level for twelve months. This policy came in for considerable criticism in the media.

In this note, we first review the literature and international experience to evaluate the underlying basis of the criticism. We refer to much of the criticism as popular myths because we find that it is either based on outdated thinking or has no empirical basis. At the same time, some of the criticism does provide food for thought and, together with the findings of the review, provides guidance for appropriate monetary policy setting in the current economic environment. Finally, we summarize recent economic developments and discuss what changes in monetary policy settings would be appropriate as the economy stabilizes and inflation comes down.

Addressing Common Criticisms

Criticism 1: Monetary policy should not be used when inflation is caused by supply-side factors

Some contend that as monetary policy controls inflation by reducing demand in the economy, it does not have a role when inflation is originating from a supply shock. This was the view among most economists in the 1970s when the United States, United Kingdom and other industrialized economies experienced stagflation because of the OPEC oil price shock. Economists at the time believed that a reduction in aggregate demand was the only channel through which monetary policy had an impact on inflation.

However, this view is a myth and the current thinking in this regard is much more qualified (see Bander et al. (2023) for a review and Ocampo and Ojeda-Joya (2023) for emerging market implications). The mainstream view today gives much greater importance to inflation expectations. The view is that if inflation is the result of a supply shock the central bank may tolerate some temporary over-shooting relative to its medium-term inflation target, but only if long-term inflation expectations remain firmly anchored such that second-round effects through wages and price settings remain muted. In addition, the central bank cannot take the stability of inflation expectations for granted. If it does not act decisively to combat inflation, it might itself contribute to a de-anchoring of inflation expectations as happened in the 1970s and early 1980s, necessitating a much more abrupt and destabilizing tightening of monetary policy later.

Thus, the appropriate policy depends on the economic situation in a country. In particular, if the likelihood of the inflation becoming entrenched in expectations is high, the central bank needs to act forcefully even if inflation is supply driven. In addition, an external supply shock, such as a shock to oil prices in Pakistan’s case, often leads to a depreciation of the exchange rate, resulting in further inflationary pressure. Thus, in countries like Pakistan where the exchange rate pass-through is high, the central bank may again need to react aggressively to meet its inflation objectives even if the price shock is supply driven. Moreover, in a country like Pakistan with low foreign exchange (FX) reserves and a binding balance of payments constraint, the central bank’s failure to act aggressively to a supply shock can result in exchange rate instability, which increases the danger of high inflation becoming entrenched in expectations.

Criticism 2: Monetary policy is ineffective when government borrowing dominates

Others assert that in a situation where government borrowing makes up a large part of the outstanding back credit and most of the new credit in a country, monetary policy is ineffective because government borrowing is not sensitive to the interest rate. However, the assumption that government expenditure is insensitive to interest rates does not have an empirical basis and high interest rates should exert pressure on the government to either reduce discretionary expenditures or increase revenues.

In any case, this argument is a myth because even if such conditions could reduce the effectiveness of monetary policy, as long as there is some private sector credit outstanding, monetary policy will have a dampening effect on aggregate demand. Alternatively, easing of monetary policy will increase private sector demand and thus add to inflationary pressure.

Moreover, bank credit is not the only channel through which tighter monetary policy affects demand and inflation expectations. Tighter monetary policy also lowers inflation by supporting the exchange rate, dampening property and asset prices (and hence private demand through wealth effects), and raises interest rates in the informal economy (see Agha et al. (2005) and Husain et al. (2022)).

Criticism 3: By increasing the budget deficit, high policy rates worsen inflation

Another set of critics allege that higher policy rates increase debt service cost and the fiscal deficit, which will boost demand and add to inflationary pressures. While there is some validity in this argument, there are number of other factors that must be taken into account to see how large an impact it will have on inflation (see Zoli (2005)).

First, as stated earlier, a high policy rate should encourage a prudent fiscal agent to cut its borrowing requirements and the fiscal deficit. Second, it depends on how the higher fiscal deficit is financed. If it is financed through printing money then it is more likely to be inflationary. On the other hand, if it leads to crowding out of private credit, it is less likely to be so. And third, as noted above, failure to maintain a high policy rate in face of high inflation would result in other channels of inflation coming into play, such as inflation expectations, increase in asset prices and exchange rate depreciation, which would add to inflation pressure.

Five Main Takeaways

- Monetary policy has a role even when inflation is the result of a supply shock because it limits second-round effects, reduces the risk of inflation becoming entrenched, and prevents inflation expectations from being de-anchored. When inflation expectations are not anchored and/or the danger of inflation becoming entrenched is high, the central bank needs to act forcefully.

- Moreover, where exchange rate pass-through to inflation is high and foreign exchange reserves are low, failure to act can lead to exchange rate instability and significantly higher inflationary pressures.

- Monetary policy is effective even when government borrowing dominates because it imposes a premium on fiscal discipline and controls inflationary pressures in the economy through multiple channels.

- The central bank must take into account the current stance of the fiscal authority and, if it is not prudent enough, monetary policy may need to compensate for it. This is not ideal and there are limits to how much the central bank can do but not acting can worsen the situation, both in terms of inflation and the external situation.

- Finally, the central bank should always consider the “real” interest rate. Nominal rates tell us nothing about the stance of monetary policy. For instance, if prices are generally increasing by 30 percent annually paying back 25 percent in interest does not represent a large burden on borrowers and does not adequately compensate savers. The goal should normally be to ensure that the real interest rate is positive on a forward-looking basis and preferably at least equivalent to average past practice in the country, i.e. 2 – 3 percent in Pakistan. In extreme crises, or when foreign exchange reserves are low and the external balance is vulnerable, the real interest rate may need to remain above 2 – 3 percent temporarily in order to stabilize the external accounts.

Implications for Monetary Policy Today

As the poor are worst hit by rising prices, controlling inflation has to be a major national priority. At the same time, an increase in the economic growth rate is also urgently required.

For the central bank, bringing inflation down to the medium-term inflation target of 5-7 percent over the next 18 to 24 months should be the top priority, as this is its primary objective according to the SBP Act. Once the economy is on a durable path to achieving that, the MPC can look to promoting economic activity subject to balance of payments constraints, as reflected by the foreign exchange reserves position. However, we note that a sustainable increase in the growth rate cannot be achieved simply through loose fiscal and monetary policy. It requires structural reforms.

Based on our review above, we now explore what the path of future monetary settings in Pakistan could look like. Before we do so, it is important to look back on how we got to the present situation of stagflation and extreme balance of payments pressures.

The Unraveling of 2022 and 2023

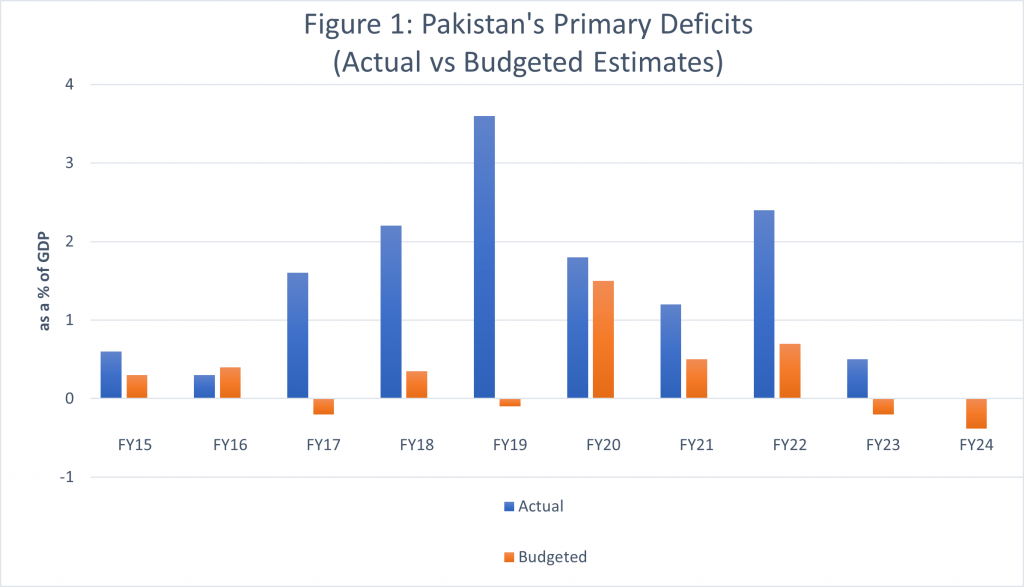

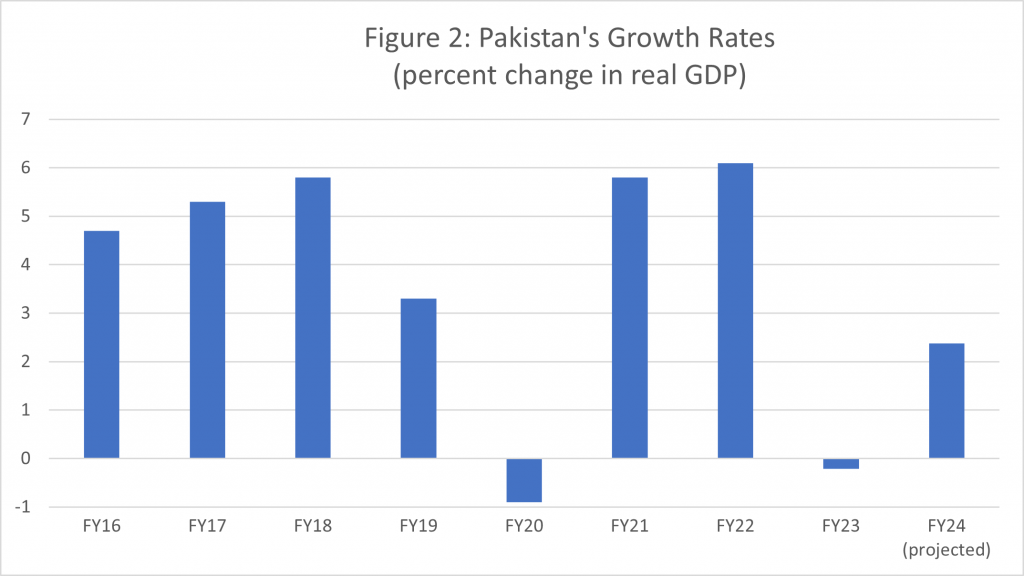

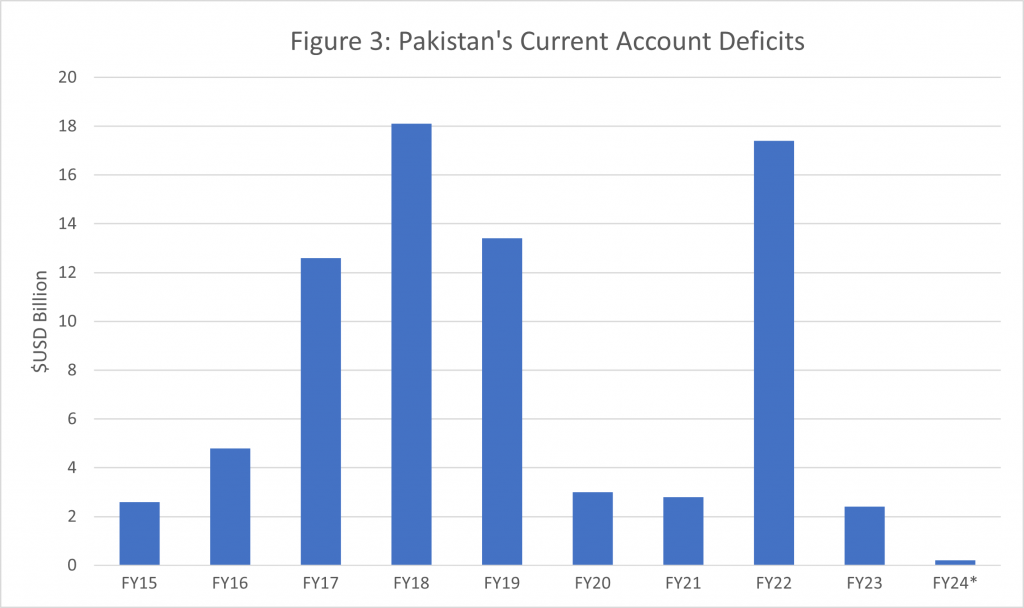

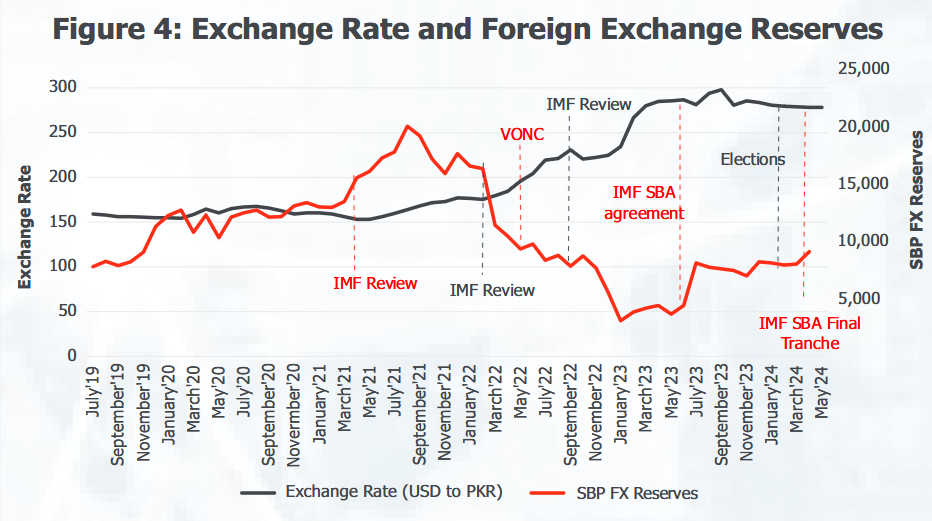

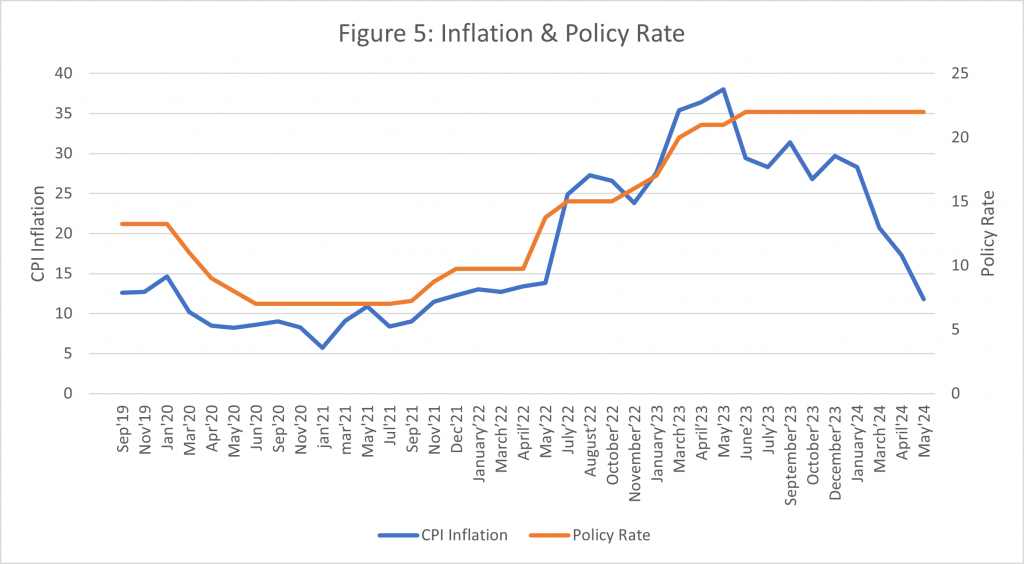

In FY 2022, after two years of prudent consolidation, Pakistan government adopted an unplanned expansionary fiscal stance that led to an overheating of the economy. The fiscal deficit increased to 7.9 percent of GDP from 6.1 percent the previous year and the primary deficit doubled from 1.2 to 2.4 percent of GDP, in complete contrast to the budgeted fiscal consolidation of around 0.7% of GDP (Figure 1). With monetary policy also loose based on the assumption that the budget would deliver consolidation, growth which had already bounced back after the COVID recession to 5.7% in FY 2021, accelerated further to 6.1% in FY 2022 (Figure 2). Coupled with the post-COVID recovery in global commodity prices, this overheating in domestic demand saw the current account deficit mushroom to $17.4 billion in FY 2022 from $2.8 billion the previous year (Figure 3), and SBP FX reserves decline from $20 billion in August 2021 to $11.4 billion in March 2022 (Figure 4). Inflation also ticked up, rising from 8.4% in June 2021 to 12.2% in February 2022 (Figure 5).

Source: State Bank of Pakistan & Ministry of Finance

Source: State Bank of Pakistan

Source: State Bank of Pakistan

*FY24 Data is for July-April

Source: State Bank of Pakistan

Source: State Bank of Pakistan

After February 2022, the economy came under pressure from a succession of severe and unanticipated shocks. First, the Russia-Ukraine war in February 2022 sent oil and food prices soaring. Second, there was extreme political uncertainty because of the “No Confidence Motion” in the National Assembly, leading to a change of government in April 2022, followed by dissolution of the provincial governments in Punjab and Khyber Pakhtunkhwa in January 2023. And third, there was acute economic uncertainty because of delays in completing reviews under the IMF Extended Fund Facility (EFF) arrangement, which led finally to the cancellation of the facility and approval of a new Standby Arrangement in July 2023.

In large part due to political and economic uncertainty, as well as lack of financing for the current account deficit, the Rupee depreciated by around 60 percent, from Rs 180 against the US dollar in March 2022 to Rs 285 by April 2023. Due to the lagged impact of two years of vigorous economic growth, the pass-through of the commodity price shock of February 2022, and the collapse of the exchange rate, inflation ratcheted up from 12.2% in February 2022 to 21.3% in June 2022 and 38% in May 2023 (Figure 5). Worryingly, inflation expectations also became un-anchored.

In response, the MPC significantly accelerated the monetary tightening cycle it had begun in September 2022, raising the policy rate by 650 basis points in FY2022 and a further 850 basis points in FY 2023. The fiscal stance also improved substantially, with the primary deficit declining from 3.1% in FY 2022 to 0.8% in FY2023. This withdrawal of monetary and fiscal stimulus helped cool demand. At the same time, with SBP FX reserves declining to an all-time low of $3.1 billion in January 2023, FX controls had to be imposed on imports.

To ensure adequate liquidity in the inter-bank market, SBP was also forced to increase the average outstanding stock of open market operations (OMOs) by Rs 3,328 billion, or 51% of the fiscal deficit in FY 2023. This was needed to ensure that market rates did not diverge unreasonably from the policy rate, especially given the large fiscal deficit, lack of external inflows for budget support, elevated economic uncertainty and panic regarding the future of the IMF program. However, it may have also contributed somewhat to the delay in inflation coming down.

Overall, economic uncertainty, tight macroeconomic policies and restrictions on imports resulted in a dramatic slowdown in economic activity and a reduction in the current account deficit to $2.4 billion in FY 2023. Growth declined from 7.2% in the 4th quarter of FY 2022 to 1% in the 1st quarter of FY 2023 and -2.7% in the 4th quarter.

Stabilization in 2024

After a nine-month hiatus, the IMF approved a US$3 billion nine-month Stand-By-Arrangement for Pakistan on July 12, 2023. General elections, originally scheduled for 2023, took place on 8 February 2024, and the new national and provincial governments are now in place. As a result, economic and political uncertainty diminished.

On the policy front, the government is implementing a prudent fiscal policy, with the primary surplus in the first two quarters larger than the corresponding period last year. Monetary policy also remains appropriately tight, with the policy rate unchanged at 22% for the last 12 months and the real interest rate positive on a forward-looking basis given forecasts of declining inflation. The exchange rate has been stable, at around Rs280 against the US dollar since March 2023, and SBP FX reserves have also stabilized at around $8 billion.

Nevertheless, inflation has generally remained high, buoyed by continuing large adjustments in administered prices of electricity and gas. In the first 7 months of FY 2024, headline inflation remained in the range of 28-30 percent but has been declining since February 2024, falling to a 30-month low of 11.8% in May 2024.

Where to from Here?

With the economy stabilizing, Pakistan negotiating with the IMF for another EFF program that should ensure fiscal discipline and provide support to the external accounts, and the “real” interest rate expected to become increasingly positive as inflation falls further, there should be scope for a cut in policy rates over time, all other things being equal.

However, there is a need to proceed with caution, especially since inflation expectations are not yet anchored around the 5-7 percent medium-term target and the experience of 2022-2023 cautions against declaring victory on fiscal discipline and external support too quickly. At this point, besides inflation, current account sustainability and exchange rate stability have to be key factors in decisions regarding the monetary policy stance. Scope to cut is contingent on fiscal policy remaining prudent, the pass-through of increases in taxes and administered prices in the budget that that will affect the path of inflation, and the external situation remaining under control under the aegis of an IMF program and adequate external financing. Finally, global commodity prices also need to be monitored, especially given on-going events in the Middle East.

In addition, the growth rate also has to be carefully watched, since rapid growth under the current economic model can quickly lead to balance of payments pressures in the form of a ballooning current account deficit and dwindling FX reserves (see Rosbach and Aleksanyan (2019)). Therefore, until structural reforms are implemented and Pakistan’s BOP-constrained growth limit is expanded, the central bank has to be even more careful once the growth rate rises above a certain prudent range.

Finally, while increasing outstanding OMOs might have been unavoidable over the last 18 months, going forward, the scale and tenor of the OMOs should be carefully calibrated. One-sided liquidity injections of a large scale and long tenors should not become a consistent, general practice as it can lead to an unwarranted increase in the money supply and add to inflationary pressures, especially as the economy recovers.

References

Agha, A., N. Ahmed, Y. Mubarik and H. Shah (2005). “Transmission Mechanism of Monetary Policy In Pakistan”. SBP Research Bulletin Vol.1, No.1.

Bandera, N., L. Barnes, M. Chavaz, S. Tenreyro, and L. von dem Berge (2022). “Monetary Policy in the Face of Supply Shocks: The Role of Inflation Expectations”. ECB Forum on Central Banking.

Husain, F., F. Hussain and K. Hyder (2022). “Monetary Policy Effectiveness in Pakistan: An In-Depth Analysis of Four Transmission Channels.” SBP Working Paper Series No.109.

Ocampo, J. and J. Ojeda-Joya. “Supply Shocks and Monetary Policy Responses in Emerging Economies”. Latin American Journal of Central Banking Vol.3, Issue 4.

Rosbach, K. and L. Aleksanyan (2019). “Why Pakistan’s Economic Growth Continues to be Balance-of-Payments Constrained”. ADB Central and West Asia Working Paper Series No.8.

Zoli, E. (2005). “How Does Fiscal Policy Affect Monetary Policy in Emerging Market Countries?”. BIS Working Papers No. 174.