A Narrow Path out of a Dangerous Place1

Is borrowing a dangerous act? Yes, as well as no! Those who borrow and invest prudently can improve their productivity and repay their debts. For them, borrowing is safe. Some, however, are unable to generate resources with which to repay their debts. For them, borrowing is dangerous. To which category does Pakistan belong?

In this note, I present a brief survey of Pakistan’s experience with domestic and external borrowing which may help the reader decide to what extent our reliance on debt has been dangerous. I begin with a brief history of Pakistan’s public debt accumulation and debt servicing.

A brief history of debt and debt service in Pakistan

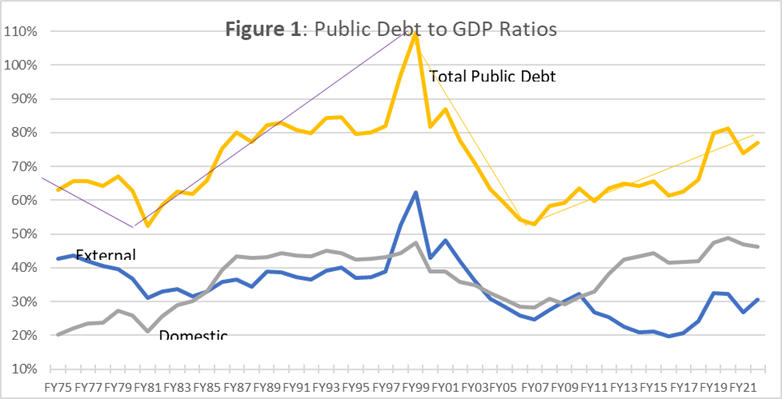

Pakistan has had elevated levels of debt at several points in its 75-year history. As far back as 1975, total debt had reached a level of 63 percent of GDP (Figure 1). While it declined for several years thereafter, it began to rise again and reached a peak of 110 percent of GDP in 1999. At this point, and for a variety of reasons, debt repayments became impossible, and a technical default was declared, followed by agreements with creditors to reschedule repayments.

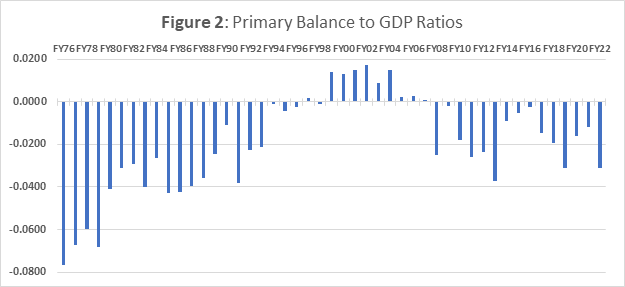

The rescheduling allowed both debt and debt servicing to decline for several years. The decline was supported by a fiscal policy stance that generated primary surpluses for nine years between FY99 and FY07. This is noteworthy as Pakistan has had only one primary surplus year outside these nine years over the entire 1975-2022 period (Figure 2). This observation draws attention to the importance of fiscal effort in managing debt.

Source: State Bank of Pakistan

1This note is based on Dr. Riaz Riazuddin’s research article “A Narrow Path out of a Dangerous Place: Debt Management and Sustainability Issues in Pakistan” coauthored with Sajjad Zaheer and prepared for the Consortium of Development Policy Research (CDPR) and Paris School of Economics.

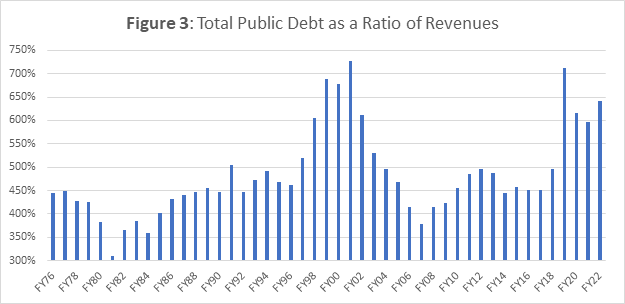

At present (FY22), Pakistan’s debt to GDP ratio stands at 77 percent, much lower than the default-inducing level of 110 percent seen in FY99. But this does not necessarily mean that the risk of default is low. Figure 3 shows that the debt to revenue ratio stands not far below now than where it was in FY99 (687 percent) when we defaulted. Once again, we are at a critical point.

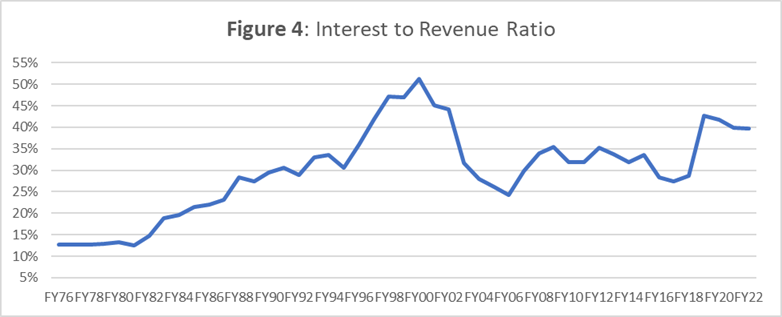

A similar picture emerges when we look at the ratio of annual interest payments to revenues (Figure 4). This flow measure shows how much of annual revenues are eaten up by annual interest payments. One can see an increase in pressure starting in FY07 when fiscal effort in terms of generating primary surpluses ended. The ratio remained elevated between 30 to 35 percent during FY08 to FY15. The next two years provided some respite with the interest burden falling between 25 to 30 percent mainly because of falling oil prices that reduced fiscal deficits and lowered borrowing requirements.

Rising international oil prices and the failure to pass on the increase to domestic oil consumers resulted in rising fiscal, debt and repayment distress from FY17 onwards culminating in the rise of interest to revenue ratio from 28.7 percent in FY18 to 42.7 percent in FY19 (prior to pandemic). Interest burden fell somewhat thereafter with steps toward fiscal consolidation to 39.6 percent but rose again due to heavy reliance on subsidies to keep domestic energy prices shielded from international price rises. The interest burden rose to 54.8 percent in FY23, even higher than the peak of 51.2 percent in FY00 when the country fell into default, once again ringing alarm bells about the sustainability of the debt.

Source: State Bank of Pakistan

Source: State Bank of Pakistan

Source: State Bank of Pakistan

Views on debt sustainability

Classical approach: The classical approach to sustainability, as articulated by Blanchard et al. (1991), emphasizes the link between sustainability and good governance. Sustainability is viewed as synonymous with good housekeeping, which involves maintaining prudent fiscal and monetary policies. The authors argue that excessive reliance on debt signals unsustainability. Sustainable fiscal policy should aim to return the debt to GDP ratio to its initial level.

The sustainability of fiscal policy is contingent upon generating future primary surpluses equal to the current level of the debt ratio. If current and future surpluses are insufficient, the government must either raise taxes or cut expenditure. Failure to do so may lead to debt repudiation and inflation. The sustainable tax rate is defined as the tax-to-GDP ratio that makes the present discounted value of surpluses equal to the current debt.

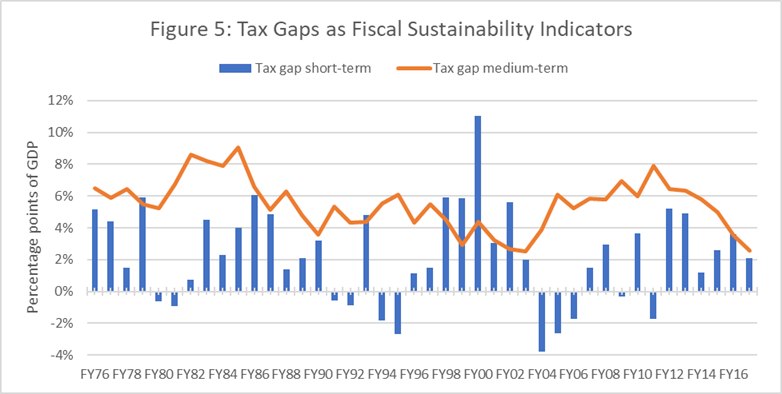

The gap between sustainable and current tax-to-GDP ratios serves as a reliable indicator of sustainability. If the sustainable ratio exceeds the current ratio, adjustments such as tax increases or expenditure cuts are necessary for fiscal policy and debt to return to sustainability. Blanchard et al. provide formulas for short-term and medium-term tax gaps based on parameters such as primary deficit, real interest rate, real growth rate, initial debt ratio, primary expenditure ratio, and tax ratio.

This analysis, applied to Pakistan, reveals that short-term tax gaps (see Figure 5) are generally lower than medium-term gaps, indicating the costs of delaying fiscal adjustments and highlighting the unsustainability of Pakistan’s fiscal accounts. Pakistan must increase its tax-to-GDP ratio by 4 to 8 percentage points to maintain fiscal sustainability.

Source: State Bank of Pakistan

IMF approach: The International Monetary Fund (IMF) employs a comprehensive Debt Sustainability Analysis (DSA) framework. This framework includes a baseline scenario with macroeconomic projections reflecting government policies. It allows for various shocks to be applied to assess debt vulnerabilities. Public debt is considered sustainable if the primary balance stabilizes debt under realistic shock scenarios.

Our implementation of the IMF DSA framework shows that Pakistan’s public debt is sustainable contingent on prudent fiscal measures, strict monetary policy, and moderate economic growth. The debt-to-GDP ratio is expected to rise initially due to fiscal relaxations but is projected to decline to around 63.1 percent by the end of the mid-term projection period, subject to government commitment with the IMF. Key factors influencing debt sustainability include real GDP growth, inflation, primary deficit, effective interest rates, and gross financing needs. The projections anticipate an average GDP growth of 2.5 percent from FY23 to FY28, with a gradual recovery following the impact of floods in 2022. Inflation is expected to decline, and the primary deficit is predicted to reduce to a surplus of 0.4 percent by FY28 due to stringent fiscal adjustments.

The analysis assumes that large gross financing needs will be met every year. This implies that Pakistan must remain engaged with the IMF for several years and adhere to prudent macro policy and structural reforms in key sectors such as energy. Any deviation from the projected policy adjustments would increase the risk of default. For example, changes in primary expenditure to GDP ratio or primary revenue could impact debt sustainability.

Debt intolerance approach: Reinhart et al. (2003) introduced the concept of “debt intolerance,” likening it to an individual addicted to milk being lactose-intolerant. In this analogy, many emerging market countries, like Pakistan, develop a penchant for borrowing despite awareness of default risks. The study, which included Pakistan among fifty-three countries, identified debt-intolerant nations with exceptionally low external debt “safe” thresholds, ranging from 15 to 20 percent of GNP. Countries with weak fiscal structures and financial systems, particularly those with a history of default or debt restructuring, were prone to debt intolerance. Such nations were also more likely to become serial defaulters.

The intensity of external debt intolerance also serves as a good predictor of domestic debt intolerance. Countries facing major debt crises often exhibited high intolerance for both types of debt. The study found that a country’s external debt intolerance could be explained by variables related to its repayment history, indebtedness level, and macroeconomic stability. Highly debt-intolerant countries were viewed as having an elevated risk of default by markets, even at low debt-to-GDP or export ratios. The paper concluded that mechanisms to limit borrowing, either through institutional changes or alterations in legal and regulatory systems, were desirable for debt-intolerant countries. The study, conducted two decades ago, remains relevant for Pakistan, which defaulted in 1998 and still displays signs of high debt intolerance.

Social welfare preservation approach: To assess sustainability, Arrow et al. (2004) proposed a criterion that intertemporal social welfare should not decrease over time. This implies that the present discounted value of net revenues less current debt need not be initially positive but should show a rising trend. While this concept is theoretically appealing, implementing it is challenging due to the lack of comprehensive social balance sheets to reflect levels of social welfare over time.

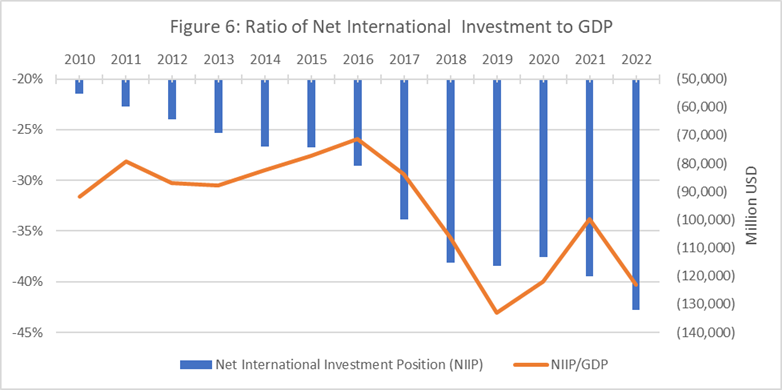

For the external sector, Pakistan has a comprehensive dataset known as the “International Investment Position” (NIIP). Despite its availability, this data is underutilized in debt sustainability analyses. The NIIP, calculated as the difference between assets and liabilities, was USD 131.9 billion in the negative at end-June 2022 (see Figure 6). While the trend improved briefly after FY16, reaching a low of minus 43.1 percent in FY19, it declined again to minus 40.3 percent in FY22. This suggests that Pakistan’s external sector is fragile according to Arrow et al.’s criteria.

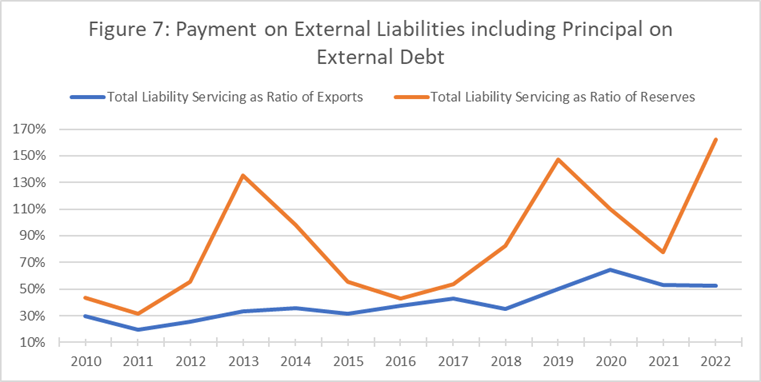

When we consider the “servicing” of all external liabilities, including not just debt servicing but also the repatriation of profits and dividends (see Figure 7), we find that the ratio of these costs to exports shows a rising trend, reaching 52.6 percent at the end of FY22. This trend, coupled with the ratio of liability servicing costs to SBP reserves, indicates increasing stress on the external sector, with the highest figure being 161.9 percent in FY22.

The above assessments imply that Pakistan needs to be very careful about further debt accumulation. Trends in key measures indicate a high risk of unsustainability. What has brought us to this pass? In the next section, we consider the extent to which debt has been transformed into productive investment in Pakistan.

Source: State Bank of Pakistan

Source: State Bank of Pakistan

Transformation of debt into productive development projects

Is raising public debt meeting its purpose? Short-term debt is raised to match the timing gap between revenues and expenditures. This should not cause debt accumulation. Long term debt is raised to finance public development projects that enhance the productivity of the economy that raise the future revenues of the government to meet its financial obligations. Has this been happening?

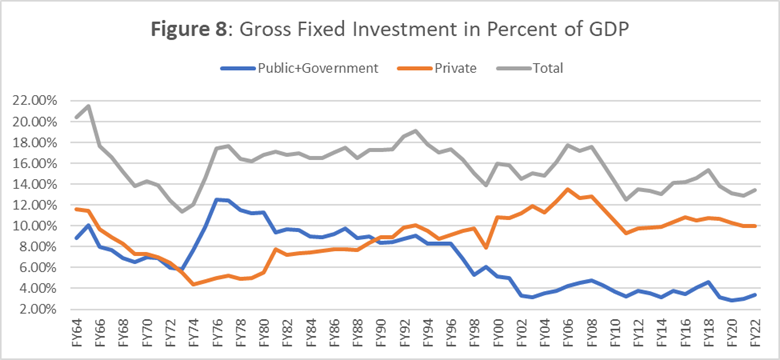

There is a declining trend in public investment, which negatively affects the accumulation of public capital stock (see Figure 8). Consequently, the portion of public capital stock attributed to long-term debt is relatively low compared to total public debt, indicating a limited transformation of long-term borrowing into productive development projects. This implies that long-term debt is increasingly used for consumption rather than for productive purposes.

Source: State Bank of Pakistan

Conclusions

Our brief review of debt history has shown that despite a rescheduling in early 2000s, Pakistan was not able to contain its fiscal and current account balances to manageable levels since mid-2000s. Although the FDI-led private fixed investment to GDP ratio rose during this period, public investment continued to decline or stagnated during this period indicating that the long-term public borrowing did not stem the declining trend in public capital. Public fixed investment stagnated since the early 2000s and its level was 3.4 percent of GDP, compared with private fixed investment to GDP ratio of 10.0 percent.

Instead of supporting public investment debt has mostly promoted aggregate consumption. This together with the increasing trend in import to GDP ratio caused several boom-and-bust episodes of growth and balance of payments crises. Fiscal profligacy was not able to post any primary surplus since FY07 and led public debt to GDP ratio to increase to 76.9 percent in FY22. While this level is lower than FY99 level of 109.7 percent, it is accompanied by close to debt distress observed then in terms of simple indicators of sustainability like debt to revenue, and interest to revenue ratios. Distress is comparably worse in terms of debt servicing to exports. All these indicators point to sustainability and liquidity problems in FY22 comparable to those observed in FY99.

We have seen that all sustainability assessments, including the IMF DSA, point to risks arising from fiscal tendencies in Pakistan relative to its debt position. The IMF approach also highlights the risks inherent in the very high gross financing requirements (around 20 percent of GDP) currently faced by Pakistan. A path out of the present dangerous position is contingent on successfully mobilizing gross financing needs and following an appropriate macroeconomic adjustment path.

References Cited

Arrow, Kenneth, Partha Dasgupta, Lawrence Goulder, Gretchen Daily, Paul Ehrlich, Geoffrey Heal, Simon Levin, et al. “Are We Consuming Too Much?” The Journal of Economic Perspectives 18, no. 3 (2004): 147–72. http://www.jstor.org/stable/3216811.

Blanchard, Olivier & Chouraqui, Jean-Claude & Hagemann, Robert & Sartor, Nicola. (1991). The Sustainability of Fiscal Policy: New Answers to An Old Question. OECD Economic Studies. 15.

IMF 2022. Pakistan: IMF Country Report No. 22/288.

Reinhart, Carmen M., Kenneth S. Rogoff, and Miguel A. Savastano. “Debt Intolerance.” Brookings Papers on Economic Activity 2003, no. 1 (2003): 1–62. http://www.jstor.org/stable/1209144.