NOTE

The 18th Constitutional Amendment re-cast the federal fiscal architecture. It deepened the devolution of administrative, political and financial authority to the provinces. As a precursor to this amendment, the resource distribution between the federal government and the provinces was finalized through the 7th National Finance Commission (NFC) Award. The enhanced share of provinces in public finances was given constitutional protection through the 18th Constitutional Amendment. However, ever since the finalization of the 7th NFC award, all the commissions constituted for formulation of new award have remained inconclusive and have only extended the 7th NFC award. The stalemate continues mainly because of the observed fiscal imbalance between the revenue and expenditure at the federal level and unwillingness of the provinces to reduce their shares. This article tries to qualify the existence of structural fiscal imbalance under a counterfactual (aspirational) model where revenues follow the incremental increase envisaged under the NFC 2009 report. The analysis finds out that the fiscal imbalance exists under the current revenue efforts and expenditure pattern. However, with improved revenue efforts (modelled on the NFC 2009 targets) Pakistan’s budget deficit drops from observed average of 6.8% of GDP during fiscal year 2011 (FY11) to FY23 to an average of 3.6% of GDP while expenditure remains constant. Thus, the argument that the 7th NFC award has inherently resulted into fiscal unsustainability weakens in face of the state underperforming on revenue generation. The article also links the significance of increased revenue generation with the political re-settlement of fiscal federalism and posits enhanced national fiscal effort as a necessary condition for the feasibility of provinces agreeing on a reduction in their share in public finances.

Introduction

In 2010, Pakistan embarked on a path of significant fiscal and administrative decentralisation. The 18th Constitutional Amendment significantly curtailed the responsibilities of the federal government and expanded the legislative and executive domain of the provinces. At the same time, it gave a more prominent role to the Council of Common Interests (CCI) in coordinating joint federal provincial tasks, and tasked provincial governments with further devolution of key functions to local governments, including lower tier governments such as municipal authorities. This devolution was protected by a stipulation that the revenue share of the provinces in each National Finance Commission (NFC) Award cannot be less than the share given in the previous Award.

Implementation of the 18th Constitutional Amendment was enabled by the Seventh NFC Award, which significantly expanded the provincial share of public finances through such actions as: (i) increasing the provincial share in the divisible tax pool from about 47.5 percent in FY2009/10 to 56 percent in FY 2010–11 and to 57.5 percent from FY 2011–12; (ii) expanding the divisible pool of federally collected taxes by reducing the federal government’s collection charge from 5 to 1 percent of divisible pool tax collection by FBR; and (iii) moving the General Sales Tax (GST) on services from the divisible pool to the exclusive domain of the provinces.

In the 14 years since this fiscal decentralisation was initiated, there have been on-going political and policy debates about the equity and efficiency of the newly decentralised fiscal regime. This article provides evidence on two of the main challenges of the regime – fiscal sustainability and political intractability – and highlights the need for increased fiscal efforts at the national level to meet these challenges.

Challenge One: fiscal sustainability

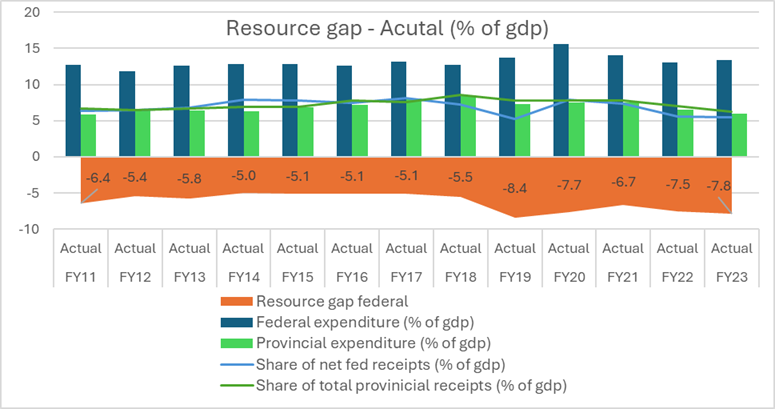

Since the passage of the 18th Amendment, Pakistan has had persistent fiscal deficits. Although revenues received by provinces have been roughly in balance with their expenditures since FY2011, there has been a persistent gap between the federal share of revenues and federal expenditures. As shown in Figure 1, provincial revenue and receipts have tracked closely to their expenditures (in green) while federal revenue has fallen far short of expenditures (in blue). The resultant federal fiscal deficit (in amber), averaged 5.8% of GDP per annum from FY11 to FY23 (fiscal deficit peaked at 8.4% of GDP during FY19, followed by 7.8% of GDP during FY23). Coupled with factors such as low GDP and export growth, this has led to Pakistan’s facing high risk of debt distress, with credit rating agencies Fitch assigning only a CCC investment grade in December 2023.

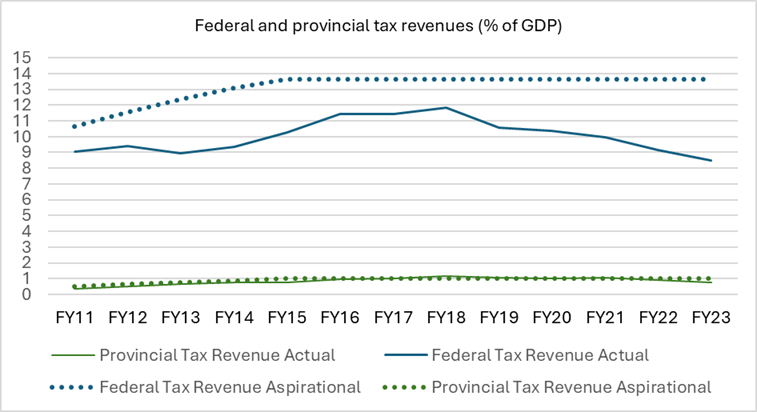

Initially, it was envisaged that both the Federal Board of Revenue (FBR) and the provinces would progressively increase their tax efforts to reach revenue ratios of 13.25% of GDP and 1.15% of GDP respectively by FY15. This did not happen. Figure 2shows that while provincial tax revenues rose from 0.36% of GDP in FY11 to 0.8% of GDP in FY 23, Federal efforts have fallen far shorter, having reached 11.8% of GDP in FY18 but then having declined to only 8.5% of GDP by FY23. Approximately 98% of the shortfall in actual tax revenue generated versus revenue generation aspiration was accounted for by shortfalls at the federal level.

Figure 1: Government revenues and expenditures split by federal versus provincial governments, and overall fiscal deficit (% of GDP)

Figure 2: Federal and provincial revenue collection versus aspiration

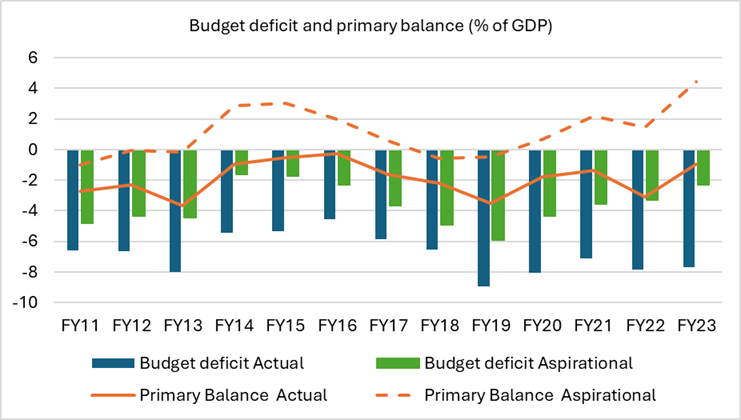

Failure to generate revenue as anticipated at the time of the 7th NFC has been a major driver of fiscal un-sustainability. If revenue had been generated as anticipated, the fiscal deficit could have been substantially decreased over the period. Figure 3 follows the assumptions of the 7th NFC (Table 1) to produce a simplified aspirational counterfactual of what the consolidated (federal plus provincial) fiscal deficit could have been if FBR and provinces had achieved their revenue generation aspirations (till the FY15 and sustained thereafter), and if additional resources generated because of the increased tax effort had been used to offset the budget deficit with expenditures remaining the same[1].

Table 1: Projection of tax receipts under the 7th NFC Award (% of GDP)

| 2009-10 | 2010-11 | 2011-12 | 2012-13 | 2013-14 | 2014-15 | |

| FBR taxes | 9.30 | 10.30 | 11.20 | 12.00 | 12.70 | 13.25 |

| Surcharges | 0.90 | 0.80 | 0.8 | 0.70 | 0.60 | 0.60 |

| Provincial taxes | 0.50 | 0.65 | 0.80 | 0.90 | 1.00 | 1.15 |

| Total | 10.70 | 11.75 | 12.80 | 13.60 | 14.30 | 15.00 |

| FBR tax effort for year | 1.00 | 0.90 | 0.80 | 0.70 | 0.55 | |

| Provinces’ tax effort | 0.15 | 0.15 | 0.10 | 0.10 | 0.15 |

Source: Table 4.2 of the NFC Report 2009.

Figure 3: Total and Primary consolidated federal and provincial governments budget deficits, actual versus simplified aspirational counterfactual

The analysis shows a substantial improvement in budget deficit and primary surplus under the simplified aspirational counterfactual. For example, in FY23, a primary surplus of 4.4% of GDP would have ensued against the actual realized primary deficit of 0.1% of GDP. On average from FY11 to FY23, Pakistan’s average budget deficit was worth 6.8% of GDP, whereas in the simplified aspirational counterfactual where all revenue generation targets had been met and expenditure remained constant, this analysis suggests it might only have been around 3.6% of GDP, on average. Cumulatively, this would amount to around 40% of GDP lower cumulative fiscal deficits, a significant amount compared to Pakistan’s total debt stock of 74.8% of GDP.[2]

While most of the ‘missing’ revenue generation has been at the federal level, there remains significant scope to increase revenue generation at both federal and provincial levels. According to the World Bank, Pakistan has a tax generation capacity of 22 percent of GDP.[3] This suggests an untapped tax capacity of around 13%[4]. Although the 7th NFC only set a provincial revenue aspiration of 1.3% of GDP, reasonable estimates suggest that provincial taxes could add a further 3% of GDP to tax revenue. The WB estimates that provincial agriculture income tax can be increased to 1% of GDP (by reducing the current 12 and ½ acre tax exemption threshold), while reforming provincial property taxes could generate up to 2% of GDP of tax revenue. As a reference, during FY20, a volume of PKR 82 billion[5] (0.2 percent of GDP) was declared as exempted agriculture income tax in the annual income tax returns filed with FBR. This indicates the minimum room for improvement in agriculture taxes. The remaining 10% of GDP tax generation gap is likely at the federal level, with possibilities to generate taxation by reducing the tax expenditures[6], taxing the retail sector, and improving enforcement of FBR[7]. The federal government could also make fiscal effort by reducing spending in line with the decentralised fiscal framework, as spending on federal ministries focused on devolved subject areas such as health and education amounted to 0.5% of GDP in FY22.

Under Pakistan’s decentralised fiscal framework provincial governments are disincentivised from taking on the political cost of generating more revenue from devolved taxation sources because their priority spending needs are already met through taxes received from their share of the federal divisible pool. This disincentive seems relevant, as even though provinces can keep and spend 100% of revenue generated through these devolved taxes, they have so far not raised significant tax revenue this way. The 7th NFC horizontal distribution (for shares between provinces) provides only a counteracting incentive, since it includes a 5% weight for taxation effort, but this is a relatively small consideration when compared to the 82% weight for population.

The disincentive for tax revenue generation is likely more even significant at federal level. There is a distortion from the fact that under the 7th NFC vertical distribution (to determine the federal share of the divisible pool), the federal government only receives 42.5% of revenue it generates from taxes in the divisible pool. This i) makes it difficult to generate large sums of money which can be spent at a federal level, for example to pay interest on Pakistan’s large federal debt or to respond to a future national emergency, ii) inhibits the government’s ability to use fiscal policy as a macroeconomic policy lever, because nearly 60% of the impact of a tight/loose federal fiscal policy will be offset by automatic impacts of provinces increasing/reducing spending, iii) reduces the political incentive for the federal government to raise taxes in these areas, since it only determines where a minority of this money is spent, and iv) creates an incentive to skew federal tax efforts to areas outside the divisible pool (for example, increasing petroleum development levy), which may harm economic efficiency.

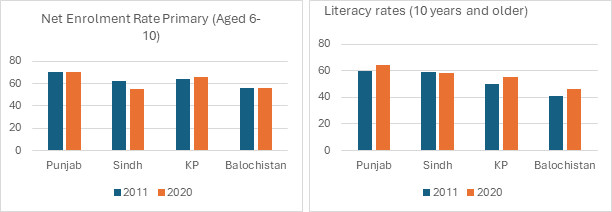

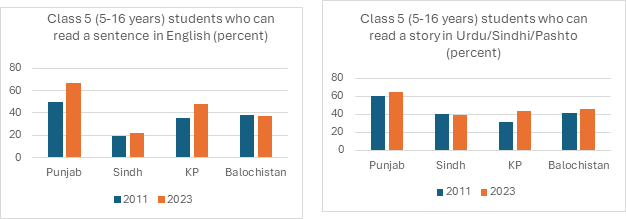

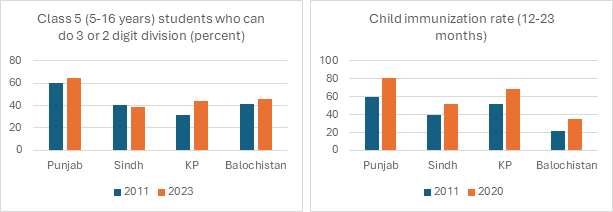

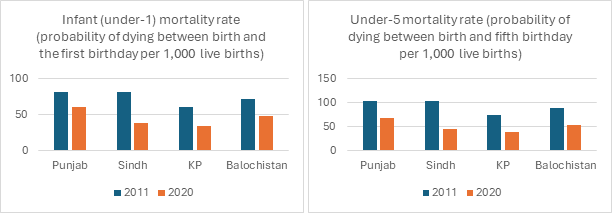

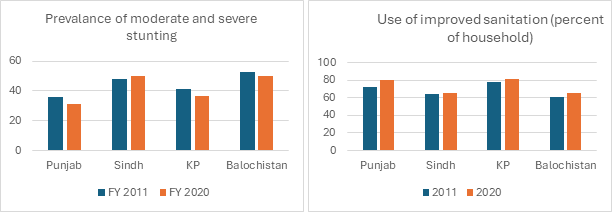

Basic service delivery is one of the key economic justifications for fiscal decentralization, but progress has been made in only a few areas. Some improvements have been made, notably with respect to child immunization rate, infant and under-5 mortality rates. However, overall social outcomes with respect to basic services (education, health, sanitation) did not improve amid gradually increasing levels of resources to the provinces (Figure 4). There are also notable differences across provinces in these outcomes. For example, in primary education, Punjab and KP have demonstrated some improvements on the margins, in learning levels in English and Arithmetic. But progress overall on other health and education outcomes has been very slow. Though not a sufficient condition for improved social outcomes, part of the 18th constitutional amendment that prescribes the provincial governments to devolve political, administrative, and financial responsibility and authority to the local governments (Article 140A of the Constitution), has remained largely incomplete. A dysfunctional local government system with weak (or in some cases, non-existent) accountabilities of the local representatives could not improve basic service delivery.

Figure 4: Progress on social outcomes after the 7th NFC Award

Source: Pakistan Social and Living Standard (PSLM) Surveys 2010-11 and 2019-20; Annual Status of Education Reports (ASER) 2011 and 2023; Multiple Indicators Cluster Surveys (MICS), various issues; [8]

Challenge Two: Political intractability

A second key challenge is that the last NFC Award (7th) announced in 2009 and implemented from 1st July 2010 has not been revised since, despite a constitutional requirement to update the NFC every five years. Time and again, deliberations on formulation of a new award have been initiated, but no agreement on a new distribution was possible. Broadly, the contentious issues are at two levels. Firstly, the provinces want an increase in the provincial share beyond what they currently get which is 57.5% of the divisible pool. This is called the ‘vertical distribution’. The federal government, on the other hand, has little motivation to do so because it considers the existing distribution to have already created a structural imbalance in favour of the provinces. Secondly, the distribution of the provincial share among the provinces is contentious because each province seeks to change the formula for its own benefit[9]. This is called the horizontal distribution. The failure to update the NFC award even only to use the latest census data for population[10], poverty and backwardness means it fails to respond to the realities on the ground in the interests of promoting equity.

Three other policy disagreements have also proved intractable. These are 1) Joint financing of federal initiatives: the federal government considers its current share to be insufficient to meet its expenses, including debt servicing obligations and social protection payments, and wants the provincial governments to cover some of the federal expenditure. The provincial governments have resisted this request. 2) Provincial responsibility for federal development/capital projects: the federal government also wants provinces to take responsibility for funding development projects that are included in the federal government’s Public Sector Development Programme (PSDP). Yet provinces are unwilling to take on funding for federally directed projects. 3) Tax reforms: provincial governments believe that federal tax administration requires reform and want a greater say in these reforms to secure a larger share of the divisible pool. The federal government however believes that provincial governments need to focus more on increasing their own tax base and improve collection of their own source revenues.

Conclusions and Recommendations

- There is scope for both provinces and the federal government to increase fiscal effort. There is roughly 10% of GDP of untapped tax capacity at the federal level, and around 3% at provincial level, in addition to significant scope for expenditure savings. Since neither provincial or federal governments will want to make a disproportionate contribution towards reaching the primary budget surpluses Pakistan needs for economic stability, negotiated and coordinated efforts are needed to solve the collective action problem.

- Government should constitute a new NFC, to consider reforms both to increase equity and efficiency. At a minimum, the new NFC could use the latest census data on population, poverty and backwardness as a crucial means for ensuring that any new award responds to the realities on the ground.

- Renewed NFC negotiations are much more likely to succeed in a context of increasing revenues.A consensus on a changed formula became possible in the 7th NFC when the overall share of the provinces was increased significantly, so that even though Punjab got a smaller share from the provincial portion, its overall share from the total tax pool increased. The fact that the 7th NFC Award persisted over the last fourteen years shows that a change in the status quo is not supported by the political economy surrounding NFC. To break the stalemate, significant changes in the taxation regimes at the provinces and the federation could help. Once such reforms start to bring results and the size of the resource pool increases, the discussions about the formulae of NFC and distribution between federal and provinces might see meaningful progress. Accelerating ongoing work on tax regime and administration reforms to grow the size of the divisible pool will lower the zero-sum stakes of the current negotiations and promote the chances of negotiations reaching a constructive conclusion.

- Tax shortfalls relative to aspirations have been far greater at the federal level, Improving incentives for federal fiscal efforts should thus be strongly considered as part of a national conversation on the decentralised fiscal framework.

[1] The estimated fiscal deficit in the aspirational counterfactual is biased upwards as it does not account for lower costs of servicing debt, which would in fact have been lower in this scenario, creating fiscal nor any broader macroeconomic channels through which tax generation and expenditure interact. The large deficits observed have necessitated higher financing needs resulting into higher debt servicing payment in the latter periods. Under the counterfactual aspiration, lower debt servicing and/or productive investment earlier in the period would have reduced deficits later in the period, but this is not accounted for in these estimates given.

[2] Summary.pdf (sbp.org.pk). As of June 2023, the gross public debt stock was 74.8% of GDP (domestic debt: 46.2% of GDP)

[3] World Bank (2023), ‘Reforms for a Brighter Future: Policy Note 6 – Strengthening Government Revenues’

[4] World Bank’s estimated 22% tax capacity less the existing (end FY 23) tax/GDP of 9.2%.

[5] Data sourced from FBR.

[6] FBR’s Tax Expenditure Report 2022 (p.8). According to this report tax expenditure was 2.7 percent of GDP during FY22.

[7] FBR’s Tax Gap Report 2022 (p.8). The report estimated the compliance gap to be 2.9% of GDP.

[8] The data for baseline year (2011) was not available for all the provinces and therefore, data for the closest outer years have been used. In case of health outcome, data for base year has been sourced from: (i) Punjab MICS 2011;(ii) Sindh MICS 2014; (iii) KP MICS 2016-17; (iv) Balochistan MICS 2010 (for stunting in Balochistan Pakistan National Nutrition Survey 2011 is used).

[9] Punjab for example is reluctant to reduce the weight of the population (82%) in the formula, all the other provinces push for the weight of other factors like poverty (10.3%), inverse population density (2.7%) and revenue collection (5%) to be increased.

[10] The formula still uses the 1998 census data, despite two subsequent census carried out – 2017 and 2023.