NOTE

Pakistan’s persistently large and growing fiscal deficit owing mainly to low tax collection is posing risks to fiscal sustainability. Consistently low tax to GDP ratio is attributable to more than one ailment in the tax system such as fragmentation of the tax base, complexity of tax system, distortive exemptions and administrative inefficiencies. Low tax revenues constrain resources available for priority investments, including in human capital. There are inherently distortive tax expenditures in the system, officially recorded as worth at least 4.41 percent of GDP for FY23, which means significant parts of the economy are not taxed at appropriate levels. There are politically sensitive distortionary tax expenditures not included in in official estimates which roughly accounts for at least another 1 percent of GDP. There are distortions in tax contribution from different sectors of economy with sectors contributing more to GDP paying less taxes and vice versa. There is inequity in tax collection patterns from different groups of taxpayers with more burden on the easier to tax segments and less focus on broadening of tax base. Pakistan’s Commitment to Equity (CEQ) revealed that in cash terms and relative to pre-tax incomes, the poorest 10 percent of the population in Pakistan pays a greater share of income in taxes than the richest 10 percent. Factors such as inequity in the tax system; anti-export bias in tax policy; and complexity in tax administration; erode tax morale, increase cost of doing business and curtail tax compliance. After capturing most crucial ailments to Pakistan’s tax system, this article gives recommendations for improving progressiveness of the tax system through reforms in three baskets i.e. tax policy reforms, automation and improved governance.

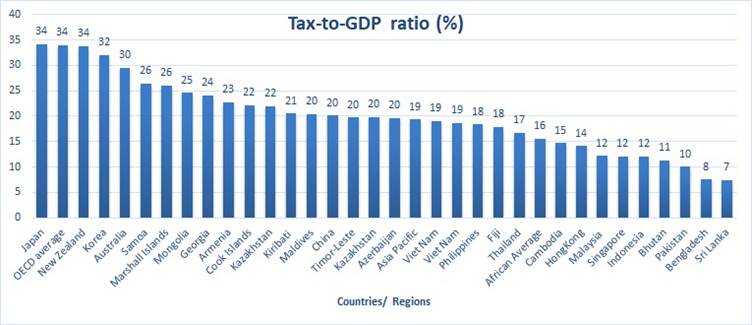

Pakistan’s economy is lightly taxed.

Pakistan’s federal tax-to-GDP ratio has hovered around 10 percent (maximum of 11.6 percent and minimum of 8.5 percent) in the last 25 years[1] due to fragmentation of the tax base, complexity of tax system, and many exemptions and administrative inefficiencies. This is lower than the average for lower middle income countries as well as much below the World Bank’s estimate of tax potential of 22 percent[2].

Graph 1- Tax to GDP ratio country comparison, OECD, 2022

Low tax collection is at the heart of Pakistan’s economic crisis:

Low tax intake over the years has meant Pakistan has had to borrow to meet expenditures. Sustained fiscal deficits, reaching a recent high of 7.4% of GDP in FY23/24[3], have by now created a mountain of debt. This coupled with factors such as low GDP and export growth has led to a high risk of debt distress and made it difficult to invest in key areas of development including human capital. Under-investment in Pakistan’s people has meant that forty percent of children under five suffer from stunted growth, leading to crippling and irreversible impacts on their cognitive and physical capacity[4].

Why is tax collection so low?

There are several reasons for this. Let’s start with tax expenditure or the amount of tax not collected because of exemptions given to various entities, businesses and entire sectors. Such tax expenditures were officially recorded as worth at least 4.41 percent of GDP for FY23[5]. Tax expenditures at the federal level rose from 1.3 percent of GDP in FY16 to 3.87 percent of GDP in FY22[6]. The largest recipients of these exemptions are independent power producers (IPPs) which get income tax and sales tax exemptions under sovereign agreements; and petroleum products which get exemptions on sales tax. Another important contributor is income tax exemption, including exemptions on business income of non-profit organizations, on high-end pensions, and agriculture income[7]. A plethora of notifications and annexures to statutes provide multiple exemptions and concessions to different sectors, categories of goods, services, and persons.

Politically sensitive tax expenditures not included in this estimate very likely account for at least another 1 percent of GDP. Based on publicly available estimates of assets and revenues, un-taxed commercial income of government-owned entities is around PKR 300 billion per annum. Not included in the tax expenditure report are exemptions worth 550 billion PKR for the real estate special regime, and 300 billion PKR for the special retail regime[8]. Furthermore, the existing analysis very likely underestimates the total as it does not account for undervaluation of rental values of properties.

Some pay more than others, and some don’t pay at all

Variations in tax rates mean sectoral taxes are highly distortionary. The manufacturing sector’s contribution to GDP is 13.6[9] percent whereas its contribution to direct taxes is 35 percent (58% if we add indirect taxes) [10]. In contrast wholesale/retail sector adds just 4 percent to direct tax collection despite their share in GDP being 18 percent[11]. Meanwhile, while real estate assets represent 60 to 70 percent of the country’s wealth, 35 percent of capital formation[12] and 8,2 percent of GDP [13], the federal tax collected on real estate is just 1.9% percent of total tax collection.[14]. While growth in this sector can boost allied industries, it is often compromised by investments in empty plots without productive linkages. Property tax collection at the sub-national level is even more dismal at 0.03 percent of total tax collection[15]. Finally, the agriculture sector is almost one-fifth of the economy (22.4 percent of GDP)[16] and generates more than USD 60 billion or Rs. 9 trillion worth of gross income annually. But its tax contribution is alarmingly low, just 0.002 percent of the total[17].

These policies contribute to the significant distortions in Pakistan’s economy, which cumulatively generate economic losses worth around 40 percent of GDP[18].

Graph 2- Sector-Wise Contribution to GDP and Tax in Pakistan

Source: Footnote 10 to 18

The World Bank has shown that tax policy distortions lead to an inability in Pakistan to allocate talent and resources to the most productive uses and may even disincentivize some needed changes.[19]. For example, capital gains on investments in land or real estate are largely un-taxed but investments in manufacturing or services face corporate profit tax rates in the range of 20 to 39 percent.[20] As a result, investors choose to channel resources into real estate rather than into manufacturing or services.

Other ailments in Pakistan’s tax policy

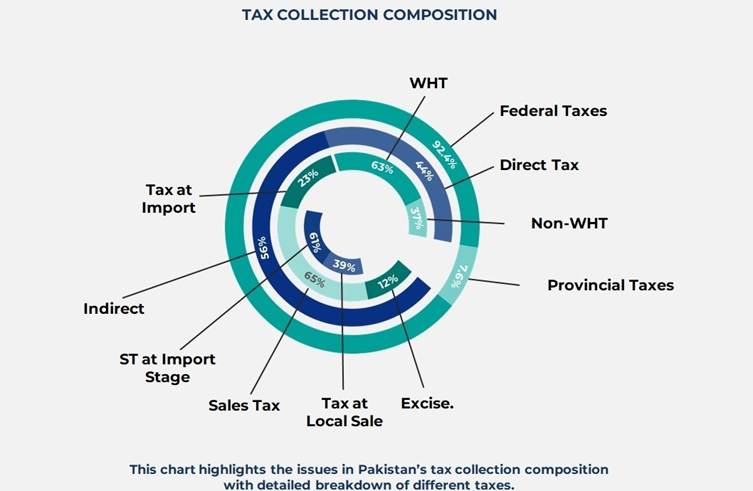

The tax base remains narrow and those who are in the tax net are burdened excessively. The current tax policy is largely focused on the collection of more and more revenues through ad hoc rate increases[21]. Tax revenues are collected overwhelmingly at the federal level, accounting for 92.4 percent in FY 23-24[22]. Provincial revenue collection is less than one percent of GDP and only around 7.6 percent of total tax collection[23]. Federal tax collection relies heavily on indirect taxes on consumption, including sales tax, customs duties, and excises. Almost 56 percent of federally collected taxes are indirect, making the system extremely regressive[24]. Pakistan’s Commitment to Equity (CEQ) revealed that in cash terms and relative to pre-tax incomes, the poorest 10 percent of the population in Pakistan pays a greater share of income in taxes than the richest 10 percent[25]. Direct taxes account for only the remaining 44 percent, with a major chunk ie 63 percent comprising various withholding taxes on documented transactions[26]. Roughly 61% of General Sales Tax (GST) on goods is collected at the import stage[27], a mode which is easier to tax but at the cost of disincentivizing manufacturing and export growth.

Graph 3- Federal and provincial tax collection

Source: Footnotes 23-28

A significant part of income tax is collected from large corporates, which disincentivizes formalisation of businesses. There are exceptionally high duties on raw materials, ranging from 52 to 90 percent.

Policy flaws in sub-national property tax collection include outdated property valuation tables; taxation based on rental value instead of the capital value of properties; and multiple exemptions and preferential treatments within the property tax regime. In agriculture, over 90 percent of farmers are un-taxed due to their land holdings falling below the 12 ½ acre exemption threshold[28]. Agricultural land used for non-agricultural purposes continues to be taxed under the agricultural income tax scheme.

Pakistan’s tax policies are also bad for exports:

Some tax policies contribute to an anti-export bias. Collection of GST at the import stage and high tariffs on raw materials reduces the competitiveness of goods made in Pakistan. Both import duties and turnover taxes add to the cost of doing business and cannot be refunded easily on exports.[29]. These policies also cause an increase in smuggling[30] . Similarly, visibility gaps in the sales tax chain lead to fraudulent refund claims which add to the cost of doing business and create avenues for rent-seeking[31].

Tax administration has its problems

Tax administration remains complex and reinforces non-compliance. Pakistan ranks 161 among 190 economies for “paying tax” indicator in the 2020 Doing Business Report[32]. Furthermore, the latest Federal Tax Ombudsman Report 2022 reveals a 63 percent annual increase in fresh complaints received by the Ombudsman office[33] . Multiple withholding taxes (WHT) add to compliance costs. Eliminating these could save around PKR 11.14 billion in compliance costs and PKR 0.24 billion in FBR collection costs, potentially leading to greater reinvestment and higher overall tax collections[34]. The current withholding tax regime is more burdensome and costly than in the rest of the world, with 283 hours required annually for tax-related tasks in Pakistan versus the global average of 108 hours[35]. This is partly due to an excessive number of payments during the year. There are various administrative issues in subnational property tax collection; assessment and recovery procedures being manual and discretionary; huge chunks of urban properties remaining out of the definition of urban property as the database is not updated regularly, and tax administration having been fragmented between civil and military organizations (cantonment boards). Agricultural income tax is also marred with administrative challenges such as a lack of integration amongst local tax administrations, and archaic methods of tax collection.

Pakistan’s fiscal federalism framework poses challenges to tax reforms. The tax base is fragmented among FBR and 12 provincial revenue departments (three for each of the four provinces). This is due to the constitutional distribution of subjects amongst federal and provincial governments; federal excise, customs duty and sales tax on goods are collected at the federal level; while provinces collect taxes sales tax on services, agriculture income tax and property tax. The disjointed structure, inconsistent laws, and overlapping jurisdictions, make it harder for citizens to comply with tax laws and rather easier to evade these, and renders tax administration more challenging for governments.

What could be done?

Tax reforms can be clubbed in three main buckets:

Tax policy reforms:

- Make income taxes more equitable and efficient by taxing all types of income. This could include abolishing withholding taxes on transactions that are not a close proxy of income, taxing pensions beyond a certain threshold and bringing business incomes of non-profit organizations into the tax net.

- Special/ fixed tax regimes for sectors could be eliminated: moving towards re-drafting of provincial agricultural income tax law to ensure that net agricultural income is subjected to the same rate schedule as applicable to other incomes. Revenues equivalent to around 0.1 percent of GDP could be generated by closing regressive corporate tax exemptions[36].

- Adjust agricultural income taxation in provinces. To generate revenue, the current 12 ½ acre tax exemption threshold could be refined to bring more agricultural land into the tax net and reduce incentives for tax evasion through breaking up land holdings. Appropriate categorization of land needs to be undertaken to bring it closer to the normal income tax regime, taking account of size, location, irrigation status, and area-based productivity aspects into tax rates.

- The reform of property taxation policies and administration could generate significant tax revenues at the sub-national level. This can be achieved by aligning property valuation tables to current market values on a bi-annual basis (currently even the gain within four to five years remains un-taxed due to the non-revision of valuation tables). Government could prioritize revaluation of annual rental values and proceed later to using capital value instead of rental value for taxation. The focus could be on improving the policy and legal framework to ensure that growing peri-urban settlements outside current notified municipal boundaries are also subject to appropriate land taxation. At the federal level, taxation of capital gains on real estate could be applied without the sunset clause.

- Tax the complete value chain of goods and services for GST. Taxing the whole value chain for GST can help documentation of the economy, make the refund system more efficient, and reduce the anti-export bias from largely collecting at the import stage.

- Removal of special tariff regimes and reduction in tariff barriers by committing to a simple and transparent tariff structure with low average tariffs and minimum dispersion would ultimately contribute to the removal of anti-export bias.

Automation:

- Focus on digitalisation initiatives to tackle tax evasion, cut down the cost of paying taxes and increase revenues. International evidence and experience can guide Pakistan’s initiatives. Digital solutions employed by the Georgia Revenue Authority have resulted in an increase in revenue generation by 50-60 percent[37]. E-invoicing increases reported firm sales, purchases, and VAT liabilities by over 5 percent on average in the first year after adoption[38]. Use of Artificial Intelligence and Machine Learning technologies for improving audit systems, tax compliance and tax filing processes can also cut down cost of paying taxes and contribute to revenue generation. In Armenia, the use of AI/ML predicts audits with above 90 percent accuracy and fraud with above 70 percent accuracy[39]. Facilitation through AI Chatbot & instructional videos can improve compliance by reducing the cost of tax compliance, as implemented by Peruvian and Mexican tax authorities[40].

- Pakistan’s digitalisation initiatives could incorporate further initiatives[41] such as import scanning, remote monitoring of retail goods, production monitoring through video analytics, development of a single portal for the sales tax[42], digitization of land records, digital imagery of urban and rural lands, redesigning of revenue authorities’ online services using semi prefilled returns, use of data-based prompts and nudging to improve tax filing[43].

- Incorporate non-government data to facilitate compliance and audit. Incorporating data from banks, utilities, state entities, airlines, property registries and provincial revenue authorities can broaden the tax net, broaden tax service penetration, and improve tax compliance. This approach is already being implemented in Indonesia.

Improved tax governance:

- Consolidate sales tax administration with a single agency, with revenues continuing to be distributed according to the National Finance Commission formula. A recent World Bank estimate suggests that further rate and base harmonization complemented by administration reforms could yield up to 1.75% of GDP in revenues[44].

- Reform the human resource of tax agencies. Significant progress can be made, including through strategic resource planning and knowledge management and insulation from political interference. Financial incentives and strengthened accountability can also be implemented.

- Separate tax policy and administration functions, leaving policy with respective provincial and federal governments but combining administration under one national tax agency. Sweden’s National Tax Board/Regional Tax Authorities’ structure is a good example of decentralization within a central system. This would remove perverse incentives in revenue collection.

References

[1] https://data.worldbank.org/indicator/GC.TAX.TOTL.GD.ZS?locations=PK

[2] Pakistan | Reforms for A Brighter Future: Policy Note 6 – Strengthening Government Revenues (worldbank.org)

[3] Ministry of Finance, ‘Federal Budget 2024/2025’

[4] https://data.worldbank.org/indicator/SH.STA.STNT.ZS?locations=PK

[5] https://download1.fbr.gov.pk/Docs/202362214627163TaxExpenditureReport2023-Final-20-6-23.pdf

[6] https://pide.org.pk/research/a-critical-appraisal-of-tax-expenditures-in-pakistan/

[7] https://download1.fbr.gov.pk/Docs/202362214627163TaxExpenditureReport2023-Final-20-6-23.pdf

[8] https://cdpr.org.pk/policy_brief_state_t/understanding-informality-in-the-wholesale-retail-and-real-estate-sector/

[9] https://www.finance.gov.pk/survey/chapter_24/3_manufacturing%20and%20mining.pdf

[10] https://www.pbc.org.pk/wp-content/uploads/Contours-of-a-New-Industrial-Policy.pd

[11] https://www.dawn.com/news/1808455

[12] Javed, U., Asad, S. A., & Sarwar, H. A. (n.d.). Informality in real estate sector. Pakistan Business Council

[13] https://finance.gov.pk/survey/chapter_24/1_growth.pdf(this includes taxes on real estate related activities and taxes on construction related activity)

[14] Javed, U., Asad, S. A., & Sarwar, H. A. (n.d.). Informality in real estate sector. Pakistan Business Council

[15] Data derived from Annual Budget Statements of federal and subnational governments.

[16]https://www.finance.gov.pk/survey/chapter_22/PES02-AGRICULTURE.pdf

[17] Data derived from Annual Budget Statements of sub-national governments

[18] World Bank (2023), ‘Reducing Distortions in the Allocation of Resources and Talents a Must to Sustain Stronger Growth in Pakistan’

[19] Benhassine,Najy; Kherous,Zoubida; Mohib,Saiyed Shabih Ali; Do Rosario Francisco,Maria Manuela.

Pakistan’s – Country Economic Memorandum : From Swimming in Sand to High and Sustainable Growth – A Roadmap to Reduce Distortions in the Allocation of Resources and Talent in the Pakistani Economy (English). Washington, D.C: World Bank Group. http://documents.worldbank.org/curated/en/099820410112267354/P1749040fc80a70ca0b6f70f7860c4a1034

[20] Income Tax Ordinance 2001

[21] Khalid, M., & Nasir, M. (n.d.). Tax structure in Pakistan: Fragmented, exploitative, and anti-growth. Pakistan Institute of Development Economics

[22] https://www.finance.gov.pk/fiscal/July_June_2023_24.pdf

[23] Ibid

[24] ibid

[25] https://commitmentoequity.org/datavisualization/country/IND

[26] Ibid

[27] https://download1.fbr.gov.pk/Docs/202467146210695FBRYearbook2022-23(Finalupdated)05-06-2024new.pdf

[28] Reforms For A Brighter Future: Policy Note 6 – Strengthening Government Revenues (worldbank.org) Page 3 of 5 Policy Brief to facilitate discussion – DRAFT MAY 2024

[29] Ahmad, E. (2006). Political Economy of Tax Reform for SDGs. India Observatory Working Papers (IOWP06). London School of Economics and Political Science. Retrieved from https://sticerd.lse.ac.uk/textonly/india/publications/working_papers/IOWP06-Ahmad.pdf

[30] National Transport Research Centre. (1986). Report on Smuggling in Pakistan

[31] Ahmad, E. (2006). Political Economy of Tax Reform for SDGs. India Observatory Working Papers (IOWP06). London School of Economics and Political Science. Retrieved from https://sticerd.lse.ac.uk/textonly/india/publications/working_papers/IOWP06-Ahmad.pdf

[32] The World Bank’s Ease of Doing Report 2020

[33] The Federal Tax Ombudsman Report 2022, Pakistan

[34] Pakistan Institute of Development Economics. (n.d.). Growth inclusive tax policy: A reform proposal.

[35] Nasir, Muhammad, Faraz, Naseem, and Anwar, Saba (2020). Doing taxes better: Simplify, open and grow economy. (PIDE Policy Viewpoint 17:2020) Page 4 of 5 Policy Brief to facilitate discussion – DRAFT MAY 2024

[36] Reforms-for-a-Brighter-Future-Discussion-Note-6-Strengthening-Government-Revenues.pdf (worldbank.org)

[37] Georgia-Digital-transformation-journey.pdf (oecd.org)

[38] UNU WIDER GRD

[39] PowerPoint Presentation (oecd.org)

[40] Pakistan-Reforms-For-A-Brighter-Future-Policy-Note-6-Strengthening-Government-Revenues. – World Bank

[41] Pakistan-Unlocking-Private-Sector-Growth-through-Increased-Trade-and-Investment-Competitiveness.pdf (worldbank.org

[42] Bellon, M., Dabla-Norris, E., Khalid, S., & Lima, F. (2022). Digitalization to improve tax compliance: Evidence from VAT e-Invoicing in Peru. Journal of Public Economics, 210, 104661.

[43] PowerPoint Presentation (oecd.org) Page 5 of 5 Policy Brief to facilitate discussion – DRAFT MAY 2024 tax authorities

[44] Pakistan-Reforms-For-A-Brighter-Future-Policy-Note-6-Strengthening-Government-Revenues. – World Bank