Tax compliance in Pakistan remains a persistent challenge, with low tax-to-GDP ratios and widespread evasion across various sectors. Whether it’s income tax, sales tax, or property tax, businesses and individuals often find ways to under-report or avoid taxes. This limits government revenue and undermines essential public infrastructure, healthcare, and education services. While much of the focus has traditionally been on enforcement, behavioral insights offer a complementary approach to encourage voluntary compliance by reshaping social norms and simplifying tax processes.

Why Tax Compliance is Low

Cultural attitudes and deep-rooted distrust of government institutions shape Pakistan’s tax compliance. Citizens often view taxes as a burden, mainly because they fear their contributions will be misused due to corruption. Trust in government is critical to tax compliance in many low-income countries. In Pakistan, this distrust, combined with a lack of transparency on how tax revenues are used, creates a norm of non-compliance. This is compounded by a visible normalization of tax evasion, where businesses and individuals observe others avoiding taxes without significant consequences. When people believe that others evade taxes without repercussions, it reinforces the perception that evasion is acceptable and the norm. This is particularly problematic in Pakistan’s large informal economy, where many undocumented economic activities make tax evasion relatively easy.

Leveraging Behavioral Insights

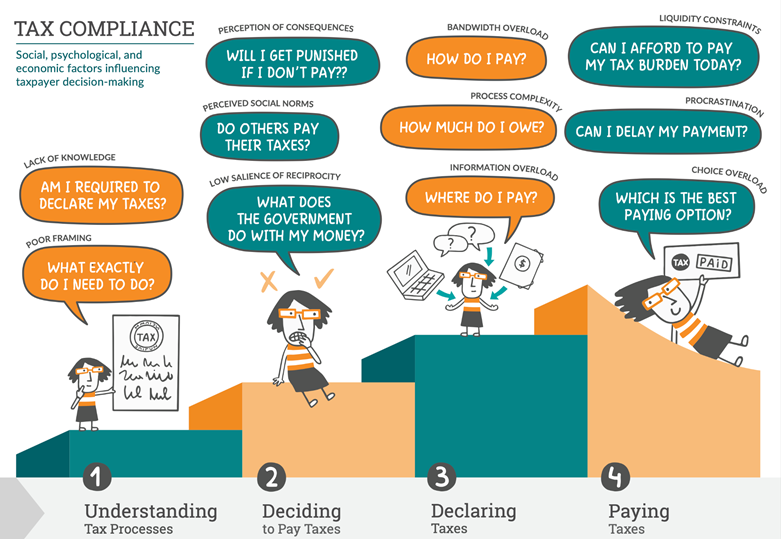

The picture below breaks down the key social, psychological, and economic factors that affect taxpayer decision-making at various stages of the tax process. It highlights how taxpayers face several barriers, from understanding their tax obligations, which are often complicated by a lack of knowledge and unclear communication. Next, the decision to pay taxes is influenced by social norms and perceptions of reciprocity—whether others are paying their taxes and whether the government provides visible benefits. Once the decision is made, taxpayers encounter logistical challenges such as process complexity and information overload when declaring taxes. Finally, liquidity constraints, procrastination, and choice overload can deter compliance even at the payment stage. The illustration emphasizes various challenges that may impact tax compliance. Behavioral insights offer a powerful toolkit for improving tax compliance by addressing all these barriers and reshaping how people engage with the tax system.

Source: Behavioral Insights for Tax Compliance’, eMBeD brief Washington, D.C., World Bank Group

Leveraging Behavioral Insights to Shift Social Norms

Behavioral economics has documented that changing social norms around tax compliance is crucial to creating a culture where paying taxes is seen as a civic duty rather than a burden. By altering social norms, paying taxes can become a collective responsibility and expected behavior, crucial for strengthening public services and improving overall governance. One way to achieve this shift is through public awareness campaigns that link taxes directly to visible public goods like healthcare and education, demonstrating how tax revenues improve citizens’ lives. Another strategy is highlighting the tax compliance of influential figures, thereby creating social pressure for others to follow suit. Transparency and accountability in government spending are also critical. When citizens see their taxes being used effectively, trust in institutions grows, making it easier to cultivate tax compliance as a norm.

Engaging Citizens to Improve Tax Compliance

Engaging citizens directly can help improve compliance. When citizens understand how taxes fund public services like healthcare and education, they are more likely to support tax compliance and demand the same from peers. Research in other contexts, such as Latin America, has shown that increased citizen engagement, including participatory budgeting and public awareness campaigns, can significantly improve tax morale. In Pakistan, citizen engagement could be deepened through community-driven initiatives, such as participatory budgeting, where citizens help decide how local tax revenues are spent. This could foster a greater sense of ownership and transparency, encouraging individuals and businesses to see taxes as beneficial rather than burdensome.

Research by Khan et al. (2022) shows that when citizens are made aware of a direct connection between their taxes and the public services provided in their neighborhoods, their willingness to pay taxes improves. They found through a large-scale study conducted in urban centers in Punjab that interventions such as earmarking a portion of property taxes for local services and directly involving citizens in decision-making about allocating these funds helped strengthen the social compact between the government and the citizens. This led to a notable, albeit modest, increase in tax payments and improved attitudes toward public services. However, they also noted that raising awareness was crucial to the intervention’s success—many citizens remained unaware of these efforts, which limited the full potential impact on tax compliance.

Incentivizing Compliance Through Consumer Involvement

Behavioral interventions that directly involve consumers can also improve business compliance. In Brazil, for example, lottery schemes, where consumers submitted receipts for a chance to win prizes, significantly increased business compliance. Consumers, acting as informal auditors, put pressure on businesses to issue receipts, reducing the opportunity for tax evasion. Pakistan could adopt a similar scheme, encouraging consumers to demand receipts and participate in lotteries that reward them for doing so. This would make businesses more accountable and raise awareness among consumers about the importance of taxes in funding public goods.

FBR and PRA have attempted consumer lottery schemes, where consumers can submit receipts for a chance to win prizes, aiming to increase business compliance and reduce tax evasion. However, the effectiveness of these initiatives remains unclear due to a lack of comprehensive evaluation. These programs could be more widely promoted to improve their efficacy, with incentives structured to sustain long-term consumer participation. Additionally, conducting rigorous impact assessments would help determine the actual effect of these schemes on tax compliance, guiding future adjustments or expansions.

The Role of Social Pressure

Social pressure is a powerful tool in shaping behaviors. Tax authorities could publicly recognize compliant taxpayers while publishing the names of defaulters. This dual strategy can create a stronger compliance incentive by combining rewards and consequences. By turning tax compliance into a socially desirable action, individuals and businesses alike are more likely to fulfill their tax obligations voluntarily. Waseem et al. (2022) found that the FBR’s public disclosure of tax payments and social recognition programs led to a significant increase in tax compliance in Pakistan. These results demonstrate the effectiveness of combining public recognition with disclosure in enhancing compliance. Pakistan could expand these efforts by improving visibility and ensuring sustained participation from both businesses and individuals.

Simplifying Tax Processes for Higher Compliance

A significant barrier to compliance is the complexity of tax processes. Recent efforts, such as introducing the IRIS portal, the Tax Asaan app, and digital payments, have made filing somewhat more accessible, but more can be done. While these digital solutions have the potential to simplify tax filing, they need to be maintained at the highest quality to ensure their effectiveness. Many users experience bugs or glitches in these systems, and there is often a lack of timely support to resolve issues, discouraging their use. To encourage compliance, these digital platforms must be designed with user experience in mind and maintained with robust technical support. Ensuring they function smoothly and reliably will reduce the administrative burden, especially on small businesses, making the tax system more accessible and increasing voluntary compliance.

Importance of Evidence-Based Policies

While these interventions—such as public recognition, lottery schemes, and behavioral nudges—are promising, they are not a one-size-fits-all solution. Various tax authorities in Pakistan, including the FBR and provincial bodies, have already implemented some of these strategies but without any scientific evidence of their success or failure. Without that evidence base, it is impossible to understand what worked and what didn’t work.

Testing and evaluation are critical for ensuring these ideas work effectively in Pakistan’s unique context. Successful interventions in other countries have been grounded in rigorous evaluation. In Pakistan, these behavioral interventions should be rigorously tested through randomized controlled trials (RCTs) or other scientific methods. This would help identify why specific approaches failed and allow for adjustments. For example, were consumers unaware of the lottery scheme, or was there insufficient incentive for businesses to comply? Systematic evaluation provides insights that can be used to improve these interventions and tailor them more closely to Pakistan’s realities.

Furthermore, a continuous learning process is essential. The dynamic nature of taxpayer behavior—shaped by economic, social, and political shifts—requires ongoing monitoring and feedback loops. Regular testing and adaptation ensure that interventions remain effective and relevant, adapting to changing circumstances.

In this process, academics and independent researchers should play a central role. By collaborating with tax authorities, they can bring scientific rigor to the design and evaluation of interventions, helping to analyze data and provide insights into long-term strategies for improvement. This partnership ensures that interventions are evidence-based, contextually appropriate, and can deliver sustained results. Testing and evaluation are not optional but essential for turning these promising ideas into scalable, impactful solutions. Without this rigorous approach, even the best-intentioned interventions risk falling short of their potential to improve tax compliance and increase government revenue.