Increasing Productivity in Pakistan through a Gender and Vulnerability Lens[1]

Summary

Clustered just above the poverty line, a large share of low income households is vulnerable to economic shocks and can slip back into poverty[1]. Government of Pakistan (GOP) has responded to the shocks with targeted support to vulnerable households. The report,[2] on which this brief is based, argues that reducing vulnerability to shocks also requires lowering the health cost associated with poor quality of air and water (addressed in a separate brief[3]) and increasing income opportunities for women.

In vulnerable households, multiple income earners help to increase household income and hence resiliency. Though more women work in the lower income quintiles than the higher ones to augment income, they engage in informal, often low-pay, work, and may not be compensated at the same rate as men. Further, their access to finance is very poor. Hence multiple earner households do not benefit at the same level with a woman earner as with men earners.

However, female employment has proven developmental impacts, both for the women themselves and for their dependents. For instance, women who work in Pakistan are more likely to have a say in household consumption decisions and their own health decisions, including the decision to use contraception.[4] Similarly, when women are part of household decision making, households tend to spend more on young girl’s education than the average household.[5]

Societal norms may discourage women from working as household income rises, and the need to augment household income decreases. Yet, when women set up a business in a household with other business(es), evidence from female microbusiness owners in Punjab suggests that overall household income is greater, and businesses are larger with more potential to grow.[6]

Research in Pakistan suggests that major challenges to women’s participation in the workforce include: (i) financial exclusion and lack of access to finance; (ii) inadequate skills, including low digital literacy; and (iii) lack of safe transport options. The overarching constraint appears to be social norms. Women usually require permission to work from other household members (including to leave the home). Some work is also considered inappropriate or unsafe for women.

Changing this mindset will require a concerted push to include women in the workforce at all income levels. Pakistan’s female labour force is currently amongst the lowest in South Asia. One estimate suggests that closing this gender gap in labour force participation could lead to a one-off 30% boost in GDP.[7]

This suggests that a broad-based agenda to bring women into the labour force could yield multiple benefits, including increasing resilience of vulnerable households, raising national productivity, and resulting in broader development and welfare gains.

- Introduction

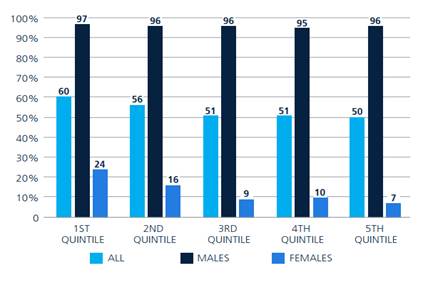

While labour force participation for men is high, labour force participation by women is substantially lower and among the lowest in South Asia, at under 30%. Further, there is considerable variation in female participation across income quartiles, ranging from 24% for the lowest quartile to only 7% for women from the highest income quartile (see Figure 1).

Figure 1. Female Participation by Income Quintile

Notes: The graph plots female labour force on the y-axis and income quintiles, disaggregated by gender, on the x-axis. Source: Cho, Y. and Majoka, Z., 2020. Pakistan Jobs Diagnostic: Promoting Access to Quality Jobs for All.

The country loses out both in terms of untapped productive potential, but also the broader development gains and resilience that comes with women wage-earners in the household. According to one estimate, closing the gender gap in labour force participation could lead to a (one-off) 30% boost in GDP.[8]

- Analysis and Findings

Data suggests that women from vulnerable households in Pakistan work because they need to augment income (PSLM 2019-2020, based on author’s calculations). Nearly a third (33.75%) of the households in Pakistan have more than one income earner, of which nearly half (43%) have at least one earning woman in the family. Multiple-earner households report a significantly higher monthly income: an average of PKR 34,000 compared to PKR 14,000 earned by single earner families. Multiple-earner households where women also work earn PKR 5,000 more than single-earner families (PSLM 2019-2020, based on author’s calculations). This may be because women tend to engage in informal, often low-pay, work, and may not be compensated at the same rate as men.

However female employment has proven development impacts, both for the women themselves and for their dependents. For instance, women who work in Pakistan are more likely to have a say in household consumption decisions and their own health decisions, including the decision to use contraception.[9] Similarly, when women are part of household decision making, households tend to spend more on young girl’s education than the average household, and as much as 13% more than the expenditure on boys.[10] A recent evaluation of BISP indicates that the grant, given to women, led to substantial decrease in child labour in the household, with greater decrease in hours worked for girls than for boys.[11]

Societal norms may discourage women from working as household income rises, and the need to augment household income decreases. However, evidence from a sample of female microbusiness owners in Punjab suggests that when women work in a household with other businesses, overall household income is greater, and businesses are larger with more potential to grow.[12]

Despite low economic participation by women, many women in Pakistan express a desire to work. In 2018, the Punjab Commission on Status of Women (PCSW) conducted a survey with approximately 30,000 women and their household members, in order to understand the barriers that women face in participating meaningfully in society and the economy. The data confirmed that the productive capacity of the female labour force is underutilized. Of the women interviewed, 11% were looking for work, and of those who were working, nearly two-thirds were working part-time. The desire to work is arguably higher among educated women — in interviews with 2500 women enrolled in undergraduate studies in public arts colleges of Lahore, more than four-fifths (84%) expressed a desire to work after graduation.[13] However,even among this educated sub-sample, female labour force participation is very low.

Another rationale is that women are caretakers in the household, and long-standing socio-cultural norms and household responsibilities do not allow women to work. Indeed, 42% of the women surveyed by PCSW cited domestic responsibilities as one of the reasons for not working. However, the low labour force participation is not completely explained by domestic responsibilities: as per the 2007 Pakistan Time Use Survey, two-fifths of the women who do not work, report not having enough to do the previous day. In fact, women who work do almost as much housework as women who do not work, while also being employed.[14]

Financial exclusion and lack of access to finance are relevant challenges for female entrepreneurs. In a survey with 1400 businesswomen in Gujranwala,[15] 22% reported lack of funds to be one of the main constraints faced by business women. In the PCSW sample, less than 5% reported having access to finance. However, evidence from around the world and from Pakistan has revealed that given the other constraints faced by women, access to finance via microloans is insufficient to encourage growth, on its own.[16]

Lack of skills and knowledge – reported by 15% of the business sample in Gujranwala and by 50% of the sample of women interviewed by PCSW in Punjab – may be an important constraint on economic participation by women. Evidence from Punjab indicates that when complimented with aid in establishing market linkages, skills training for women can be particularly beneficial, leading to potentially significant increase in the yearly income and empowerment of female entrepreneurs.[17]

Social norms, regarding acceptable occupations for women and of their mobility outside the household, as well as safe transport to and from places of work, are other binding constraints on women working. More than a third of the sample interviewed by PCSW reported not having access to transport or accommodation near places of work. Many women require permission from their household members to work – approximately 35% in Punjab (from PCSW Survey 2018). Household members may not allow women to work if they deem it unsafe and inappropriate for women. For instance, data from the Labour Force Survey (2000 – 2010) reveals that a third of the women who work, work from home. Two-fifths of those who do not work, say they do not have permission from their fathers or husbands to work outside the home, 15% report dislike having to work outside the home themselves.[18]

Policy Recommendations: What can be done to encourage more participation of women in the labour force?

The recommendations below are ordered in terms of priorities that focus on benefitting women in vulnerable households. These households are the ones that seek to augment income through female participation in the labour force. Yet they do not fully benefit from this participation due to a lack of skills, low wages and gender disparities. However, as noted above, there are much broader development outcomes associated with women working. Encouraging women borrowers from these vulnerable households to put loans to productive use could reap significant development gains. It could also be a mechanism to help increase household income and shift mindsets in the immediate term, then trying to tackle gender wage disparities or encouraging formal work at low income quintile levels, which is administratively fraught with difficulty.

A push for gender balance and wage equality in formal, higher paid jobs is also necessary to shift mindsets towards greater female labour force participation. This will benefit the country from an overall productivity standpoint, but vulnerable households even more so, through helping to shift cultural norms and building greater resiliency due to an increase in income from multiple earners.

Drawing on Pakistan-specific and available literature, the following six areas could be prioritized:

1. Ensure gender related KPIs are required for all financial institutions (from banks to microcredit) that provide loans. These KPIs need to be realistic and take into account different socio-cultural conditions across the provinces. Yet they need to be monitored and adjusted upwards over time. This may require the creation of a gender-related advisory committee within Planning Commission and Ministry of Finance to recommend appropriate KPIs in line with a vision for Pakistan. The State Bank of Pakistan could, as regulator, assume the responsibility for monitoring and publicly disseminating progress over time.

Examples of such KPIs for loan programmes include the following:

- Improve monitoring with data disaggregated by gender:

- Loan applied for, and approved

- Loan size and use

- Loan disbursed

- Loan refused

- Defaults and delayed payments

- Set targets:

- Introduce a KPI for gender inclusiveness (or different KPIs for each province, considering varying societal constructs)

- Improve chances of women borrowers utilizing loan programmes:

- Overlap with existing efforts to improve digital literacy for women

- Make application process friendly for women borrowers (who may not have a cell phone)

- Develop ‘use cases’ to illustrate access and encourage take-up.

- Oversight and Advisory mechanism:

- Include better gender representation in committees overseeing loan programme progress

2. With a focus on the most vulnerable households, encourage financial institutions to develop products to attract more female borrowers. Providing more flexible capital can facilitate entrepreneurial capacity of low-income female borrowers.[19] Encouraging financial institutions to design disbursal methods that ensure that the recipient has some control over grants or loan funds can also reduce misappropriation of women’s funds. As BISP biometric verification experience has shown, allowing women some control over funds withdrawn can be an important first step in giving women a say in household decision making.

3. Reduce the stigma of a female breadwinner in target communities. This can be done through information interventions, exposure to role models, and promotion of discussions (via media campaigns and college-based programs) that discourage gender discrimination

4. Take transport related initiatives that help to reduce both mobility and safety concerns for women, so they can participate more fully in training and/or in the labour force. This could be through encouraging the development and offer of new and improved transportation options for women, including group transportation from schools, offices, factories, etc.

5. Encourage the development and implementation of skills training and mentoring programs specifically for women. Encourage educational and professional institutes to leverage interaction among working women for information and skill sharing, as well as a support system to overcome barriers to their mobility.

6. Encourage large businesses to formulate and implement gender inclusiveness policies. This could include gender KPIs across corporations but also for senior level positions, provision of childcare services to retain women in the workforce, ensure equal wages for equal work, etc.

[1] An estimated 52% of the entire population was vulnerable to falling back into poverty in 2018-2019 according to Jamal, H., 2021. Updating Pakistan’s Poverty Numbers for the Year 2019. Social Policy and Development Center (SPDC), Karachi, Pakistan.

[2] See footnote 1.

[3] Policy Brief: Prioritizing Climate Action through a Health and Vulnerability Lens also draws on the report mentioned in footnote 1 above.

[4] Fatima, D., 2014. Education, employment, and women’s say in household decision-making in Pakistan.

[5] Saleemi, S. and Kofol, C., 2022. Women’s participation in household decisions and gender equality in children’s education: Evidence from rural households in Pakistan. World Development Perspectives, 25, p.100395; Data from Pakistan Rural Household Surveys 2014, 2016, 2017.

[6] d’Adda, G., Mahmud M., Said F., and Ubfal D., 2019. Constraints to female entrepreneurship in Pakistan: The role of women’s goals and aspirations.

[7] Cuberes, D. and Teignier, M., 2014. Gender inequality and economic growth: A critical review. Journal of International Development, 26(2), pp.260-276.

[8] Ibid.

[9] See footnote 5.

[10] See footnote 6.

[11] Churchill, S.A., Iqbal, N., Nawaz, S. and Yew, S.L., 2021. Unconditional cash transfers, child labour and education: theory and evidence. Journal of Economic Behavior & Organization, 186, pp.437-457.

[12] See footnote 7.

[13] Ahmed, H., Mahmud, M., Said, F. and Tirmazee, Z., 2020. Undergraduate Female Students in Lahore: Perceived Constraints to Female Labour Force Participation. Lahore School of Economics.

[14] Field, E. and Vyborny, K., 2016. Female labor force participation in asia: Pakistan country study. Manila: Asian Development Bank.

[15] See footnote 7.

[16] Banerjee, A., Duflo, E., Glennerster, R. and Kinnan, C., 2015. The miracle of microfinance? Evidence from a randomized evaluation. American economic journal: Applied economics, 7(1), pp.22-53 and Said, F., Mahmud, M., d’Adda, G. and Chaudhry, A., 2021. Home-based Enterprises: Experimental Evidence on Female Preferences from Pakistan.

[17] Cheema, A., Khwaja, A.I, Naseer, F. and Shapiro, J.N. (2019). Skills for Market (SFM 2013-14) – Market Linkage (ML 2015-16): Final Impact Report. Available at Punjab Skills Development Fund (PSDF) website: https://www.psdf.org.pk/wp-content/uploads/2020/03/SFM-ML-Final-Impact-Evaluation-Report-1.pdf

[18] See footnote 19.

[19] Dimble, V. and Mobarak, A.M., 2019. Saving microfinance through innovative lending. IGC Growth Brief Series, 17.

[1] This policy brief draws from the report “The Path to a Successful Pakistan” prepared by a team comprising Kulsum Ahmed (Director ILM, Honorary Fellow CDPR and former Sector Manager, World Bank), Ijaz Nabi (Chairman, CDPR and Country Director, IGC and former Sector Manager, World Bank), Sanval Nasim (Assistant Professor, Colby College), Amna Mahmood (Country Economist, IGC), and Farah Said (Assistant Professor, LUMS). We are grateful to the International Growth Center (IGC) for funding.